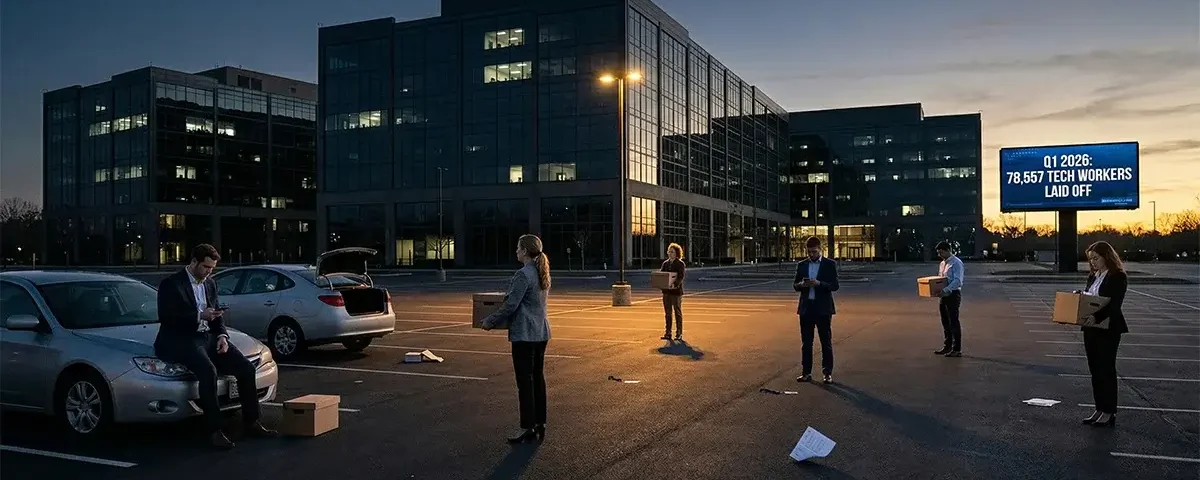

If you have opened your news feed in 2026 and found yet another headline about thousands of corporate workers losing their jobs — from Amazon to Oracle to Block to Atlassian to Salesforce — you are not imagining a pattern. The scale, pace, and breadth of workforce reductions happening right now are genuinely extraordinary. According to layoffs.fyi, 78,557 technology workers were laid off in the first quarter of 2026 alone — equivalent to 926 job losses every single day. Across all sectors, more than 1,621 companies have announced mass layoffs since January 1, 2026. The layoffs are hitting companies that are simultaneously reporting record revenues, committing hundreds of billions of dollars to AI infrastructure, and watching their stock prices rise.

This creates an obvious and entirely reasonable question: if companies are doing well, why are so many people losing their jobs? The answer is not simple — and anyone offering a single-sentence explanation is either oversimplifying or has an agenda. The truth is that the layoff wave of 2025 and 2026 is driven by at least seven distinct forces that are operating simultaneously, reinforcing each other, and producing a magnitude of workforce disruption that exceeds any single prior episode in modern corporate history. This cornerstone guide examines every one of those forces with the data and specificity that workers, investors, and policymakers need to understand what is actually happening.

The 2026 layoff wave is not primarily about companies in financial distress — it is primarily about companies in structural transition. The seven forces driving layoffs are: AI and automation displacement, capital reallocation to fund AI infrastructure, pandemic overhiring correction, management de-layering, macroeconomic pressure from tariffs and energy costs, investor pressure to expand margins, and the geopolitical and government workforce reduction. These forces overlap and compound — a company facing all seven simultaneously (as many tech firms do) produces layoffs even while revenues grow. Understanding which force is driving any specific layoff is the key to assessing how permanent the job loss is and what the re-employment path looks like.

The Scale of the Problem: By the Numbers

Before examining the causes, the scale demands a moment of honest acknowledgment. The numbers in 2025 and 2026 are not normal, even by the already-elevated standards of post-pandemic tech employment disruption.

In 2025, 245,953 technology workers were laid off across 783 separate layoff events — an average of 674 people losing their jobs every single day, for an entire year. In 2026, the pace has accelerated: 227 layoff events through early April 2026 have already affected 91,679 workers — a rate of 926 people per day, 37% faster than the 2025 pace. Across all industries (not just technology), more than 1,621 companies have announced mass layoffs since January 1, 2026. The single largest layoff event of 2026 to date is Oracle’s 30,000-person corporate reduction. Amazon has eliminated approximately 30,000 corporate roles since October 2025. Block (formerly Square) announced it would cut 40% of its workforce — approximately 4,000 employees. Atlassian reduced headcount by 10%, or around 1,600 roles. Salesforce has made multiple rounds of cuts across product management, data analytics, and marketing teams.

Perhaps most striking: nearly half of these layoffs are being attributed, at least in part, to artificial intelligence. According to Nikkei Asia’s analysis, 47.9% of the 78,557 Q1 2026 tech industry layoffs — approximately 37,638 positions — were attributed to reduced need for human workers due to AI and workflow automation. This represents a dramatic increase from 2025, when AI was cited as a factor in fewer than 8% of layoff announcements. The corporate narrative around AI as a driver of workforce reduction has shifted from taboo to mainstream in the space of 12 months.

Why Are So Many Layoffs Happening? The 7 Root Causes

Cause 1: AI and Automation Displacement — The Structural Shift

The most discussed and most consequential cause of the 2026 layoff wave is the genuine displacement of human workers by artificial intelligence and automation systems. This is real — but it is more nuanced than the headlines suggest, and OpenAI CEO Sam Altman himself has acknowledged the complexity: “I don’t know what the exact percentage is, but there’s some AI washing where people are blaming AI for layoffs that they would otherwise do, and then there’s some real displacement by AI of different kinds of jobs.”

The real displacement is concentrated in specific role categories. According to analysis from RationalFX covering 166 major layoff events in 2026, AI-driven displacement is most acute in: coordination and program management roles (technical program managers, product managers, and project managers whose core function is tracking and synthesizing information between teams — functions that AI agents now perform); content creation and editing roles (where AI writing and image generation tools have dramatically reduced the human hours required to produce equivalent output); customer service and first-line support (where AI chatbots and automated resolution systems handle an expanding share of interactions); data entry, analysis, and reporting (where AI tools execute in minutes what previously required hours of human analytical work); and basic software testing and code review (where AI coding assistants and automated testing frameworks have reduced the headcount required per engineering team).

The cost economics driving this displacement are stark. AI inference token costs have dropped 280-fold in two years. Enterprise AI infrastructure spending now exceeds $700 billion globally. As per-unit costs fall and capability rises, the financial case for AI substitution improves every quarter — meaning the displacement force is not static but accelerating. Salesforce has stated that AI handles roughly 30–50% of work in some functional areas, maintaining service levels with fewer employees. At that substitution rate across an entire department, the headcount required falls by 30–50% even as output is maintained — producing the paradox of profitable companies with high revenue growth eliminating workers simultaneously.

The roles being created to replace the eliminated ones require fundamentally different skills: AI engineers, prompt engineers, machine learning operations specialists, AI safety and governance professionals, and hybrid roles combining domain expertise with AI tooling proficiency. IBM has reportedly tripled its entry-level hiring in 2026, demonstrating that the new AI-era job market is not uniformly contracting — but the skills mismatch between the roles being eliminated and the roles being created is real, wide, and painful for workers without the specific credentials the new positions require.

Cause 2: Capital Reallocation — Turning Payroll Into Compute

The second cause of the layoff wave is financially distinct from AI displacement, though closely related: companies are converting payroll expenses into AI infrastructure investment. This is capital reallocation, not workforce redundancy — and it is being driven by the extraordinary scale of AI infrastructure commitments that the largest technology companies have made.

Amazon, Meta, Google, and Microsoft are collectively expected to invest approximately $650 billion in AI within 2026 alone — primarily in data centers, custom silicon chips, networking infrastructure, and the energy systems required to power AI training and inference at scale. These commitments represent capital expenditure levels that exceed what the companies’ operating cash flows comfortably support while also maintaining pre-AI workforce costs. The financial arithmetic creates pressure: every dollar not spent on payroll is a dollar that can flow into the AI infrastructure buildout without requiring additional debt financing.

A single Amazon L7 senior manager represents approximately $250,000–$350,000 in annual total compensation. Thirty thousand such positions represent $7.5–$10.5 billion in annual payroll expense. At Amazon’s $200 billion 2026 AI capex commitment — which exceeded analyst estimates by $53 billion — the payroll savings from its 30,000-person reduction directionally fund a meaningful fraction of the investment above the analyst consensus. This is not coincidence. It is deliberate capital reallocation, and when Amazon’s free cash flow turned negative in the quarter its capex hit record levels, the case for workforce reduction as a capital source became financially urgent.

Companies that are laying off workers while simultaneously committing to record capital expenditure are not in distress — they are reallocating. The workers eliminated are the cost basis being converted into the investment basis. This structural reallocation explains why layoffs and strong earnings reports are increasingly appearing simultaneously in the same news cycle, a pattern that confuses workers accustomed to layoffs signaling financial difficulty.

Cause 3: Pandemic Overhiring Correction — The Bill Comes Due

A third distinct cause — particularly prominent at Amazon, Meta, and Google but affecting the broader technology sector — is the unwinding of the extraordinary overhiring that occurred during the 2020–2022 COVID-19 pandemic period. This correction predates the AI investment thesis and would be happening at some scale regardless of the AI transition.

When the pandemic arrived and digital commerce, cloud computing, remote work infrastructure, and entertainment services all surged simultaneously, technology companies responded rationally by hiring aggressively to meet what appeared to be permanent demand expansion. Companies like Amazon doubled their workforces in under three years. Meta, Google, Microsoft, and dozens of smaller technology firms hired at rates unprecedented in their histories, building organizational structures to manage the new scale with management layers, program management offices, and support functions that grew proportionally with headcount.

The problem that materialized as pandemic-era tailwinds normalized — as people returned to physical retail, as Zoom fatigue set in, as the advertising market contracted — is that the organizational growth had created unnecessary complexity and coordination overhead without proportional customer value. Andy Jassy of Amazon described the dynamic precisely: “If you grow as fast as we did for several years, you end up with a lot more layers. Sometimes without realizing it, you can weaken the ownership of the people who are doing the actual work.” The layoffs that Amazon executed in 2022–2023 (27,000 positions) and again in 2025–2026 (30,000+ positions) are the two-phase correction of a workforce that expanded too rapidly to maintain the organizational discipline the company’s culture demands.

The pandemic correction is largely complete for the companies that moved earliest — Meta, for example, returned to aggressive hiring after its 2022–2023 restructuring and has continued expanding its total headcount even while cutting specific divisions. For companies that delayed the correction, including some mid-market technology firms, the unwinding is still in process in 2026.

Cause 4: Management De-Layering — The Flatness Imperative

Closely related to but distinct from the pandemic correction is a broader organizational philosophy driving layoffs across technology companies: the deliberate reduction of management layers to create flatter, faster-moving organizations with more direct ownership at the individual contributor level.

This philosophy has several drivers. First, AI tools are capable of performing many coordination and oversight functions that previously required human managers — reducing the ratio of managers required per individual contributor. At Amazon, internal targets to increase the individual contributor-to-manager ratio by at least 15% produce a mathematically predictable headcount reduction in management layers even before any other consideration. Second, the competitive pressure of AI-era technology development favors organizations that can make and execute decisions faster — which requires fewer approval layers, fewer consensus-building meetings, and more autonomous individual contributors with direct ownership of outcomes. Third, venture capitalists and institutional investors have developed a strong preference for “capital-efficient” companies with high revenue-per-employee ratios, creating financial market incentives for flatter organizational structures regardless of their operational benefits.

The target metric driving this cause — revenue per employee — is measurable and public for every company with disclosed financials. In 2026, the revenue-per-employee benchmark for high-performing technology companies has been driven dramatically higher by AI tools, with some companies achieving 50–100% revenue-per-employee improvements over 2023 levels through AI augmentation of their existing workforce. Companies that have not yet achieved these ratios face investor pressure to close the gap — either by growing revenue faster (harder) or by reducing headcount (faster). For most companies in 2026, the path of least resistance to investor satisfaction is the latter.

Cause 5: Macroeconomic Pressure — Tariffs, Energy Costs, and Recession Fear

Beyond the structural technology-sector causes, a fifth driver of the 2026 layoff wave is macroeconomic deterioration that is both independent of and compounding the structural forces already described. The US tariff regime of 2025–2026 has introduced significant cost pressure and uncertainty across manufacturing, retail, and supply chain-dependent businesses. The Iran war and Strait of Hormuz closure that began February 28, 2026 have produced the largest oil supply disruption in history — driving energy costs up more than 50% in five weeks and introducing stagflationary pressure that is compressing consumer spending and business investment simultaneously.

For companies in energy-intensive industries — chemical manufacturers, steel producers, shipping logistics, agriculture — layoffs driven by margin compression from energy costs are neither AI-related nor pandemic-correction-related: they are a direct consequence of the energy shock. Dow Chemical announced 4,500 layoffs as part of an initiative to offset surging energy and feedstock costs. Algoma Steel Group issued 1,000 layoff notices as it closed a blast furnace. Ericsson cut 1,900 jobs, including 1,600 in Sweden, as it manages a prolonged downturn in telecom equipment spending.

The macroeconomic pressure also affects technology companies indirectly: as consumers face higher gas and food prices, discretionary technology spending comes under pressure; as business confidence falls amid tariff and geopolitical uncertainty, enterprise software, advertising, and cloud service revenue growth rates slow; and as recession probability rises (Goldman Sachs currently places 12-month recession probability at 30%, while Moody’s AI model sits at 49%), risk-averse executives accelerate headcount reductions to preserve cash and improve their financial resilience before any potential downturn materializes.

Cause 6: Investor Pressure and Margin Expansion — The Shareholder Return Driver

A sixth, often underacknowledged cause of the layoff wave is the direct pressure that equity markets exert on corporate leadership through the relationship between layoff announcements and stock price performance. The pattern is consistent and well-documented: companies that announce significant workforce reductions almost invariably see their stock prices increase on the announcement day and in the following weeks. This creates a financial incentive structure in which corporate leaders who cut workers are rewarded by markets regardless of whether the operational justification for the cuts is clear.

The mechanism operates through earnings per share. When a company eliminates a meaningful percentage of its workforce, the immediate financial impact — before any revenue change — is reduced payroll expense and improved operating margins. Higher operating margins, for a company with stable or growing revenue, directly translate to higher earnings per share, which is the primary metric driving equity valuations. Block’s stock was projected to improve its operating margin by 8–12 percentage points following its 40% workforce reduction. Oracle’s stock surged following its Q3 fiscal 2026 earnings release despite (or partly because of) the concurrent 30,000-person layoff announcement.

Tom’s Hardware noted that “in almost 100% of cases, news about layoffs is met with a rise in stock prices by respective shareholders.” When markets consistently reward layoff announcements regardless of operational necessity, the incentive for corporate leaders to pursue workforce reductions as a shareholder value mechanism — independently of any genuine efficiency justification — becomes significant. This does not mean all layoffs are primarily shareholder-driven, but it does mean the financial incentive structure consistently pushes in the direction of more reductions, faster, than pure operational logic might require.

Cause 7: Government Workforce Reduction — The DOGE Effect

A seventh cause of job loss that is frequently conflated with corporate layoffs but is structurally distinct is the reduction of the US federal government workforce. In 2025, the Department of Government Efficiency (DOGE) orchestrated a reduction of approximately 71,981 government employees, with 182,528 total federal workers laid off according to layoffs.fyi data. These are not corporate layoffs in the traditional sense, but they represent a significant labor market displacement that: reduces purchasing power among government workers and contractors, affects companies in government-adjacent industries (defense technology, federal IT contracting, government consulting), and creates a signal to the broader economy that workforce reduction at scale is politically acceptable and financially rewarded.

The government workforce reduction also compounds the recession risk picture — unemployed federal workers reduce consumer spending, potentially softening demand in the industries their former purchasing supported, creating conditions that make private-sector employers more cautious about hiring and more willing to accelerate their own workforce adjustments.

The “AI Washing” Problem: When Companies Use AI as a Convenient Excuse

A critical and intellectually honest element of the layoff debate in 2026 is the “AI washing” phenomenon — the use of AI as a convenient narrative cover for layoffs that are primarily driven by other factors. Sam Altman’s acknowledgment of this pattern — that companies sometimes blame AI for layoffs they would be doing anyway — is shared by Cognizant’s Chief AI Officer Babak Hodjat, who told Nikkei: “Sometimes AI becomes the scapegoat from a financial perspective, like when a company hired too many, or they want to resize, and it gets blamed on AI.”

AI washing serves several corporate interests simultaneously. It signals to investors that management is actively embracing AI — positioning the company as forward-looking rather than merely cost-cutting. It reduces the reputational cost of layoffs by framing them as an inevitable technological transition rather than a strategic failure. It deflects attention from other causes — pandemic overhiring, poor strategic decisions, margin expansion pressure — that would reflect less favorably on corporate leadership. And it normalizes the disruption for remaining employees by framing it as a structural inevitability rather than a discretionary management choice.

How can workers and observers distinguish genuine AI displacement from AI washing? Several indicators are useful. Genuine AI displacement tends to target specific, narrow role categories that correspond directly to demonstrable AI capabilities — the roles whose functions AI tools can now perform. AI washing tends to involve broad cuts across multiple role types with only a superficial connection to AI capability. Genuine AI displacement is typically accompanied by concurrent hiring in AI engineering and integration roles — the company is actually building the AI systems that replace the human roles. AI washing layoffs are often not accompanied by proportional increases in AI hiring — the workforce reduction is the end in itself, not a transition to a different skill mix. And genuine AI displacement announcements typically include specific examples of AI tools that have demonstrably changed workflow requirements — not just a reference to “AI” as a general technological trend.

The Sectors Beyond Tech: Layoffs Are Not Just a Technology Story

While the technology sector dominates layoff headlines in 2026, the workforce reduction wave extends across industries in ways that are frequently underreported. Understanding the breadth of the layoff environment is essential for workers in non-technology fields who may believe they are insulated from the disruption.

Manufacturing and industrials: Dow Chemical (4,500 layoffs), Algoma Steel (1,000), Airbus (2,000+ globally by mid-2026), and Chevron (8,000 by end-2026) represent a manufacturing sector contending with both energy cost pressure from the Iran war and accelerating automation of physical production processes. The Iran war oil shock has compounded pre-existing margin pressure on energy-intensive manufacturers, triggering restructuring that would have happened more gradually in a stable energy environment.

Finance and fintech: Commerzbank (3,900 layoffs as part of restructuring amid a UniCredit takeover bid), fintech companies across payments and lending, and major financial services technology firms are all restructuring. The combination of higher interest rates (which affect bank profitability models), AI automation of compliance and analysis functions, and consolidation pressure is producing meaningful financial sector displacement.

Retail and e-commerce: Traditional retail has been contracting its workforce for over a decade as e-commerce displaces physical retail sales, but the pace is accelerating in 2026 as AI-powered inventory management, personalized pricing, and automated customer service reduce the headcount required to operate both physical and digital retail operations at equivalent scales.

Media and content: AI writing, image generation, video production, and audio synthesis tools are fundamentally changing the economics of content production. Media companies have faced persistent structural challenges from digital disruption for a decade, but AI tools are now compressing those challenges further by reducing the cost of content production at scale.

Healthcare administration: While clinical healthcare roles remain structurally resistant to displacement (requiring physical presence, complex judgment, and patient relationship), healthcare administration — billing, coding, prior authorization processing, scheduling, and routine patient communications — is being automated at an accelerating pace. Healthcare administration accounts for approximately 30% of US healthcare spending and employs millions of workers whose specific functions are directly addressable by current AI capability.

Which Jobs Are Safest — And Which Are Most At Risk

For individual workers assessing their own exposure to the layoff wave, the evidence across all seven causes points to a consistent pattern of which roles are protected and which are vulnerable.

Highest displacement risk profile — roles that combine all vulnerability factors:

The most vulnerable positions in 2026 share a common set of characteristics: they are primarily digital and screen-based (not requiring physical presence); they are coordination-heavy (tracking information, scheduling meetings, synthesizing reports from multiple sources, managing approvals); they can be specified in rules or prompts (their work can be described clearly enough that AI systems can replicate it); they sit in the middle management layers targeted by de-layering mandates; and they are in sectors facing AI investment pressure, energy cost pressure, or post-pandemic correction. Product managers, technical program managers, marketing coordinators, HR generalists, content writers for standard formats, customer service representatives, data entry processors, and basic code reviewers all exhibit most or all of these characteristics.

Lowest displacement risk profile — roles that are structurally protected:

The most resilient positions exhibit the opposite characteristics: they require physical presence and embodied skill in variable environments (trades, healthcare, emergency services); they depend on genuine human relationships and trust for their effectiveness (therapy, complex sales, leadership, teaching); they involve legal, ethical, or safety accountability that must rest with an identifiable human (surgery, law, executive leadership); they are in areas where AI capabilities are currently building and require human direction (AI engineering, ML operations, data architecture, AI safety); or they require original creative judgment with cultural depth that AI-generated content at scale cannot match (senior creative direction, brand strategy, original research).

The reskilling imperative: The single most consistent finding across all research on the 2026 layoff wave is that workers who develop AI fluency within their existing domain are dramatically better positioned than those who ignore or resist AI tools. PwC research found a 56% wage premium for workers who use AI effectively — meaning that in many roles, AI proficiency is not just job insurance but a direct earnings multiplier. The workers most at risk are not those whose industries are disrupted by AI — every industry is disrupted — but those who refuse to adapt to AI tools within their specific domain expertise.

What Happens Next: The Trajectory of Layoffs Through 2026

Based on the structural forces described in this guide, several developments are predictable with reasonable confidence for the remainder of 2026.

The AI attribution rate in layoff announcements will continue rising. The normalization effect is already in motion: as Block’s, Atlassian’s, and Amazon’s explicit AI attribution generated market reward without significant reputational cost, the template for future announcements has been set. Companies considering workforce reductions for any combination of the seven causes will increasingly frame them through the AI lens — making the already-difficult task of distinguishing genuine AI displacement from AI washing more challenging.

The macroeconomic pressure from the Iran war energy shock will add a new, non-AI category of layoffs through Q2 and Q3 2026 if the Strait of Hormuz situation does not resolve quickly. Energy cost-driven layoffs in manufacturing, logistics, and energy-intensive industries are already materializing and will grow in proportion to the duration of the oil supply disruption.

The Q2 2026 earnings season will be a critical inflection point. If major AI investors — Amazon, Microsoft, Google, Meta — demonstrate proportional AI revenue growth relative to their massive capex commitments, investor pressure on non-AI-investing companies to match the investment will intensify, driving the next wave of capital reallocation layoffs. If AI revenue disappoints relative to infrastructure investment — if the 10:1 capex-to-revenue gap documented in our AI bubble analysis persists — investors may turn skeptical, tightening capital market conditions and potentially triggering a different type of layoff wave driven by funding pressure on AI-dependent companies.

Practical Guidance for Workers Navigating the Layoff Environment

For the tens of millions of American workers whose jobs sit in vulnerable categories, the combination of understanding the causes and taking proactive protective action is the most effective available response to the disruption described in this analysis.

Conduct an honest task audit of your own role: List the 15–20 specific tasks you perform in a typical week and categorize each as: A (routine, digital, rule-following — highest AI substitution risk), B (judgment, relational, contextual — moderate protection), or C (physical, accountable, creative — highest protection). If more than 70% of your work is Category A, your role carries meaningful AI displacement risk and warrants proactive career planning. This is not cause for panic — it is cause for action.

Build AI fluency in your specific domain immediately: Every professional domain now has AI tools designed for it — legal research AI, medical documentation AI, financial analysis AI, marketing content AI, project management AI, code generation AI. Learning to use the tools in your specific domain is not optional career enhancement in 2026 — it is baseline competency maintenance. Workers who demonstrate AI fluency within their domain are being retained and promoted; those who do not are being targeted in reduction waves.

Understand your financial resilience position: In an environment where any role below the senior-most level in affected categories carries meaningful layoff risk, the financial buffer between a layoff notification and economic crisis is a direct determinant of your ability to navigate the transition effectively. A 6-month emergency fund — the minimum appropriate for the current risk environment — enables a deliberate, strategic job search rather than a panic-driven one. If you are below 3 months of essential expenses in liquid savings, building that buffer is the highest-priority financial action available regardless of how secure your current role feels.

Know your legal rights before you need them: The WARN Act (60-day advance notice for qualifying mass layoffs), the OWBPA (21–45 days to review severance agreements), COBRA health insurance continuation rights, and state unemployment insurance eligibility rules are all rights that exist whether or not your employer explains them to you at termination. Familiarizing yourself with these protections before a layoff occurs — rather than discovering them in the shock of the moment — materially improves your financial outcome if a reduction does affect you.

💬 0 Comments