America’s infrastructure — roads, bridges, pipes, electrical grids, and transit systems — is in a documented state of deterioration after decades of deferred maintenance and underinvestment. The American Society of Civil Engineers gave the nation’s infrastructure a C- grade in its 2025 report card, estimating a $2.6 trillion funding gap over the next decade. Yet within this national challenge lies one of the most overlooked long-term investment opportunities available to individual investors in 2026: infrastructure ETFs and related investments.

Infrastructure investments — companies that own and operate roads, bridges, airports, utilities, pipelines, cell towers, and data centers — have historically provided inflation-resistant, recession-resilient returns with higher dividend yields than the broad stock market. In a 2026 environment combining recession risk, elevated tariffs favoring domestic production, and federal infrastructure spending commitments, the infrastructure sector offers a compelling combination of defensive characteristics and growth potential.

What Is Infrastructure Investing?

Infrastructure investing encompasses companies and assets that provide essential physical and digital systems that modern society requires to function. The infrastructure investment universe divides into several sub-categories:

Transportation infrastructure: Toll roads, airports, seaports, and railroads. These assets typically operate under long-term concession agreements with governments — earning steady, inflation-indexed revenue from user fees over periods of 20–99 years. Companies in this category include Ferrovial (operator of toll roads and airports globally), Atlas Arteria, and various airport and port operators.

Utilities: Electric transmission and distribution companies, natural gas pipelines, water and wastewater utilities. These are regulated monopolies — their returns are set by state utility commissions, providing stability and predictability. Dividend yields of 3–5% are common in this sector. Major US utility ETFs include XLU (Utilities Select Sector SPDR) and VPU (Vanguard Utilities ETF).

Energy infrastructure: Midstream oil and gas companies that own pipelines, storage facilities, and processing plants. Master Limited Partnerships (MLPs) dominate this category — Kinder Morgan, Enterprise Products Partners, and MPLX pay high distributions (often 6–9% yield) from toll-like pipeline revenue that is largely insensitive to commodity price fluctuations.

Digital infrastructure: Cell towers, data centers, and fiber optic networks — the physical backbone of the digital economy. American Tower (AMT), Crown Castle (CCI), and Equinix (EQIX) are dominant players in this growing category. Data center demand has accelerated dramatically with AI infrastructure buildout in 2025–2026.

Why Infrastructure Performs Well During Recessions and Inflation

Infrastructure assets have two characteristics that make them particularly valuable in 2026’s economic environment:

Inflation resistance: Most infrastructure contracts include inflation escalation clauses — toll rates, utility rates, pipeline tariffs, and cell tower lease rates typically increase automatically with inflation indexes. Unlike a typical business whose costs rise with inflation while its ability to raise prices is constrained by competition, regulated infrastructure owners can pass through cost increases to users. In a tariff-driven inflationary environment, infrastructure’s inflation pass-through is a genuinely valuable portfolio characteristic.

Recession resilience: People continue driving on toll roads, using electricity, consuming natural gas, and relying on wireless networks during recessions. The demand for essential infrastructure services is significantly more stable than consumer discretionary spending or corporate capital expenditure. During the 2008–2009 recession, regulated utility stocks declined approximately 28% compared to the S&P 500’s 57% decline — a meaningful performance advantage in a severe downturn.

The Federal Infrastructure Investment Tailwind

The Infrastructure Investment and Jobs Act (IIJA) of 2021 authorized approximately $1.2 trillion in infrastructure spending over 5–10 years — with the majority of disbursements occurring in 2023–2027. This federal spending has created direct revenue growth for construction materials companies, engineering and design firms, and equipment manufacturers. In 2026, the IIJA spending pipeline remains active, providing a measurable revenue tailwind to companies exposed to government infrastructure contracts.

Additionally, the tariff environment of 2025–2026 has created a “domestic manufacturing premium” — infrastructure projects using domestically produced steel, cement, and equipment are favored by both policy and procurement rules. This benefits US-based infrastructure construction and materials companies specifically, creating a tariff-era tailwind that extends beyond the IIJA spending directly.

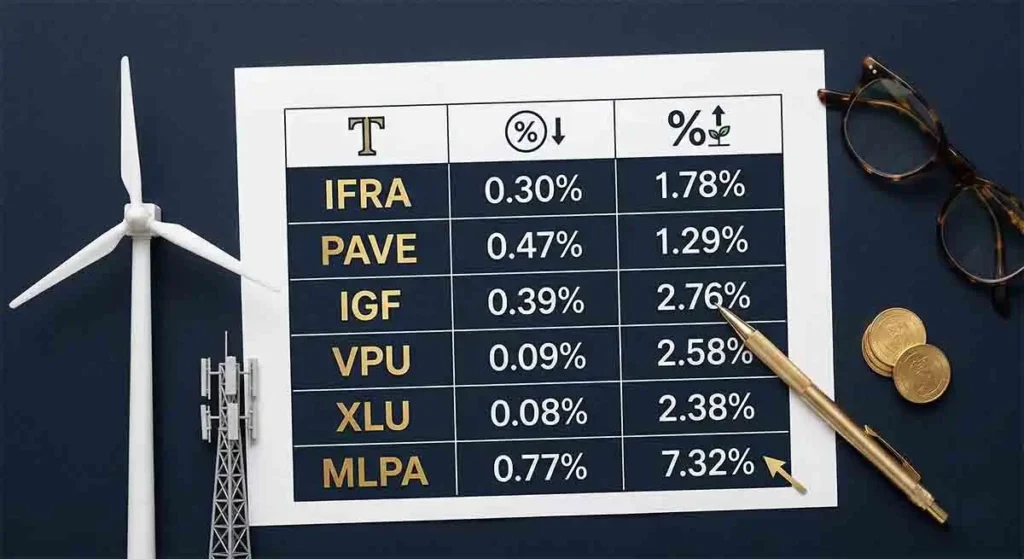

How to Invest in Infrastructure: ETF Options for Individual Investors

| ETF Ticker | Fund Name | Expense Ratio | Dividend Yield (approx.) | Focus |

|---|---|---|---|---|

| IFRA | iShares U.S. Infrastructure ETF | 0.30% | 2.8% | Broad US infrastructure including utilities, industrials, materials |

| PAVE | Global X U.S. Infrastructure Development ETF | 0.47% | 0.8% | Growth-oriented — construction, engineering, materials; lower yield |

| IGF | iShares Global Infrastructure ETF | 0.40% | 3.1% | Global infrastructure — airports, toll roads, utilities, pipelines |

| VPU | Vanguard Utilities ETF | 0.10% | 3.2% | US regulated utilities — electric, gas, water; defensive, high yield |

| XLU | Utilities Select Sector SPDR | 0.10% | 3.1% | S&P 500 utility companies — most liquid utility ETF |

| MLPA | Global X MLP ETF | 0.45% | 7.2% | Midstream energy MLPs — highest yield, energy infrastructure focus |

| AMT | American Tower REIT (individual stock) | N/A | 3.0% | Cell tower infrastructure — global digital infrastructure leader |

Infrastructure REITs: A Special Category Worth Understanding

Cell tower REITs (American Tower, Crown Castle) and data center REITs (Equinix, Digital Realty) are a uniquely positioned infrastructure subcategory in 2026. AI infrastructure buildout is driving unprecedented data center construction — Equinix and Digital Realty both reported record leasing activity in 2024–2025, driven by hyperscaler demand from Microsoft, Google, Amazon, and AI-focused companies. Cell tower REITs benefit from 5G network densification and the continued growth of wireless data consumption.

These digital infrastructure companies combine the predictable, long-term contracted revenue characteristics of traditional infrastructure with the growth drivers of the technology sector — an unusual combination that has produced strong long-term returns. Both AMT and EQIX experienced significant valuation correction in 2022–2023 when interest rates rose (REITs are rate-sensitive due to their high debt loads and dividend-focused investor base), creating attractive entry points for long-term investors relative to their growth prospects.

Risks to Understand Before Investing in Infrastructure

Interest rate sensitivity: Infrastructure assets are often valued using discounted cash flow models — when interest rates rise, the present value of long-duration cash flows declines, reducing valuations. The 2022–2023 rate increases caused significant valuation declines in utility and infrastructure stocks despite their businesses performing well operationally. In a 2026 environment where the Fed may cut rates, this risk is partially mitigated — but rate sensitivity remains a structural characteristic of infrastructure investing.

Regulatory risk: Regulated utilities and infrastructure assets depend on regulatory frameworks that can change. State utility commissions can constrain rate increases; environmental regulations can impose unexpected costs; and infrastructure concession agreements can be renegotiated under political pressure in certain markets. Geographic diversification across multiple regulatory regimes reduces this risk.

Concentration risk in pure-play infrastructure: Allocating more than 10–15% of a diversified portfolio to any single sector — including infrastructure — creates concentration risk. Infrastructure should be viewed as a complement to a broadly diversified core portfolio (total market index fund), not a replacement for it.

💬 0 Comments