When you lose your job, the American financial system offers a structured set of resources designed to help you bridge the gap to your next employment — but most people who experience job loss do not fully utilize these resources, either because they do not know they exist or because they delay claiming them out of embarrassment, optimism, or confusion about eligibility. Here is the complete guide to everything you are entitled to after a layoff in 2026.

The average laid-off worker in the US leaves $12,000–$20,000 on the table by not claiming all the benefits and protections available to them in the 90 days following job loss. This includes unclaimed unemployment insurance, COBRA versus marketplace health insurance comparison, retirement account rollover mistakes, severance negotiation opportunities, and employer benefits that expire within tight windows after termination.

Day 1–7: The Immediate Action Checklist

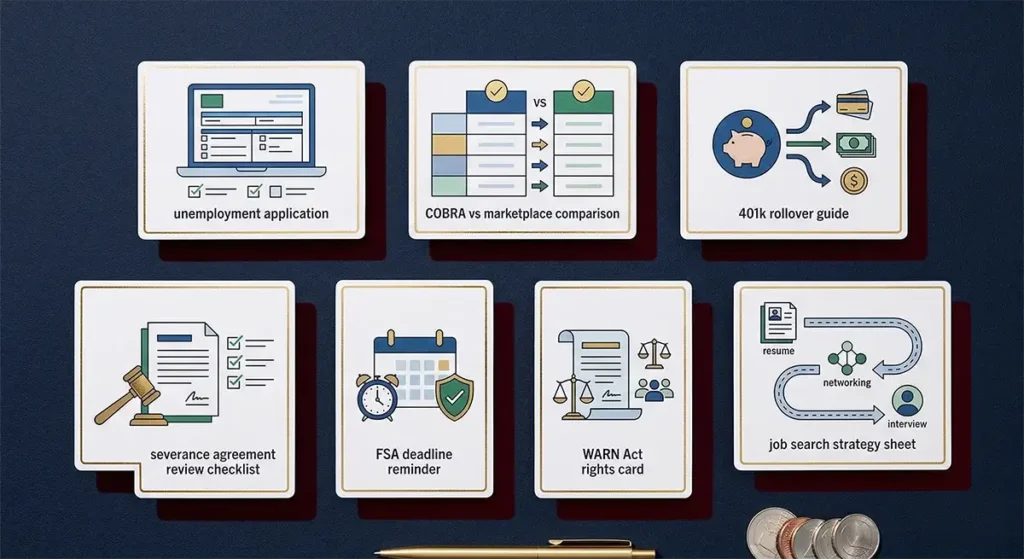

File for unemployment insurance immediately. In every state, unemployment benefits are backdated to your filing date — not your layoff date. Every week you delay filing is a week of benefits you cannot recover. File online at your state’s unemployment agency website on the same day or the day after your layoff. You will typically need: your Social Security number, your employer’s name and address, your start and end dates of employment, your reason for separation (layoff/reduction in force = you are almost certainly eligible), and your last paycheck stub or income information. The initial application takes approximately 30 minutes. Benefits typically begin 2–3 weeks after filing, following a brief waiting period.

Read your WARN Act rights. The Worker Adjustment and Retraining Notification (WARN) Act requires employers with 100+ employees to provide 60 days advance notice before mass layoffs affecting 50+ workers. If your employer laid you off with less than 60 days notice — or with no notice — and the layoff involved 50+ workers, you may be entitled to 60 days of back pay and benefits. Violations are litigated through federal court — consult an employment attorney if you believe your employer violated WARN Act requirements.

Review your severance agreement carefully before signing. Most severance agreements include a waiver of claims against your employer — meaning once you sign, you typically cannot sue for wrongful termination, discrimination, wage theft, or other employment law violations. Signing quickly is rarely in your interest. You generally have 21 days to review a severance agreement (45 days for mass layoffs involving workers over 40) and 7 days to revoke your signature after signing. Use this time to review with an employment attorney, particularly if you suspect the layoff was discriminatory, retaliatory, or involves unpaid commissions, bonuses, or overtime.

Health Insurance: Your Most Time-Sensitive Decision

Losing employer-sponsored health insurance at job loss is a qualifying life event that allows you to enroll in a new health plan outside the standard open enrollment window. You have two primary options — and the financial comparison between them is more complex than most people assume.

COBRA continuation coverage allows you to continue your current employer’s health plan for up to 18 months after job loss. The catch: you pay the full premium — what you paid as an employee plus the employer’s share plus a 2% administrative fee. The total monthly cost for a family plan under COBRA is typically $1,500–$2,200/month — a significant shock after paying only $400–$600/month as an employee with employer subsidy.

ACA Marketplace coverage may be dramatically cheaper if your income has dropped significantly due to job loss. Premium tax credits on the ACA Marketplace are based on your projected annual income for the year — and with income dropping to $0 or your expected unemployment income, you may qualify for heavily subsidized coverage or even Medicaid. A family of four with income below $40,000 in most states qualifies for Medicaid or very low-cost Marketplace coverage. Calculate your subsidy at healthcare.gov before enrolling in expensive COBRA.

The COBRA vs Marketplace decision: COBRA makes sense when you expect to be re-employed quickly (within 60–90 days), when you have specific doctors or treatments that are in-network under your current plan but may not be covered under Marketplace alternatives, or when your family has complex ongoing health needs that make continuity of care critical. For most laid-off workers, comparing Marketplace options before defaulting to COBRA saves $500–$1,500/month.

Your 401(k) After Job Loss: Critical Decisions

Your 401(k) balance does not disappear when you are laid off — but you face several important decisions about what to do with it. Options available after job loss:

Leave it in your former employer’s plan: You can typically leave your 401(k) in your former employer’s plan indefinitely if your balance is above $5,000. This is often the path of least resistance — and the right choice if your former employer’s plan has excellent low-cost investment options. However, you lose the ability to make new contributions and you can no longer take plan loans.

Roll it over to an IRA: Rolling your 401(k) to a traditional IRA at a brokerage like Fidelity, Vanguard, or Schwab typically expands your investment options, consolidates your retirement accounts, and gives you full control over your investments. Do a direct rollover (the money moves directly from your 401(k) to the IRA without passing through your hands) to avoid the mandatory 20% withholding that applies to indirect rollovers.

Roll it to your new employer’s 401(k): After starting a new job, you can roll your old 401(k) into your new employer’s plan — simplifying your retirement account management and, if your new employer’s plan has good investment options, maintaining access to potential future plan loans.

Cash it out (do not do this): Withdrawing your 401(k) balance at job loss triggers ordinary income tax on the full amount plus a 10% early withdrawal penalty (if under age 59½). On a $50,000 balance for a worker in the 22% bracket, this means approximately $16,000 in taxes and penalties — losing 32% of your retirement savings immediately. Only consider this as an absolute last resort after exhausting all other options.

Benefits That Expire Quickly After Termination

Several employer benefits have short windows after termination — claim these before they expire:

FSA Flexible Spending Account funds: If you have a healthcare FSA with unused funds, you may be able to use them for eligible medical expenses incurred before your termination date. Funds not used by the plan’s grace period or run-out period after termination are forfeited. Schedule any outstanding medical, dental, or vision appointments before your termination date if you have a significant FSA balance.

Life insurance conversion: Employer-provided group life insurance typically allows you to convert to an individual policy within 31 days of termination without a medical exam. If you have health conditions that would make individual life insurance expensive or unavailable, exercising this conversion option within the 31-day window preserves your coverage. The individual premium will be higher than the group rate but you maintain the coverage without underwriting.

Stock options and restricted stock unit vesting: If you have unvested stock options or RSUs, termination typically cancels unvested grants. Review your equity award agreement for post-termination exercise windows — many employers give only 30–90 days after termination to exercise vested options before they expire. Consult with a tax professional before exercising options, as the tax implications of stock option exercises are complex.

Accrued vacation payout: In many states (California, Illinois, and others), accrued but unused vacation time is legally considered earned wages that must be paid out upon termination. In other states, this is determined by your employer’s written policy. Review your employee handbook for the vacation payout policy and verify that your final paycheck reflects all accrued leave owed to you.

Rebuilding: The Job Search Strategy in a Recession Job Market

In a recession job market, the strategies that worked in a tight labor market require adjustment. The 2021–2022 job market rewarded passive job seekers — recruiters reached out, multiple competing offers were common, and job seekers could afford to be selective. The 2026 market is more competitive, requiring more active and strategic approaches.

The most effective job search strategies in a 2026 recession market: network first (60–80% of jobs are filled through referrals before they are publicly posted — LinkedIn and personal outreach to former colleagues and managers produces more interviews per hour invested than job board applications); target stable recession-resistant industries (healthcare, education, government, utilities, essential retail — sectors documented to maintain or grow employment through recessions); consider contract or temporary roles while searching (which maintain income, fill resume gaps, and frequently convert to permanent positions); and use your state’s American Job Center (CareerOneStop.org) for free job search assistance, skills assessments, and retraining programs funded by the Workforce Innovation and Opportunity Act.

💬 0 Comments