Every time recession fears intensify in the American financial news cycle, one question reliably surges in search volume: “Are credit unions safer than banks during a recession?” It is a reasonable question — and one that deserves a serious, data-driven answer rather than the vague reassurances or unnecessary alarm that typically characterize discussion of this topic. This comprehensive guide examines the actual safety comparison between credit unions and banks during economic downturns, drawing on historical data from every significant US financial crisis of the past century.

Both federally insured banks and federally insured credit unions are safe places for your deposits up to the insured limit — $250,000 per depositor per institution per ownership category — during any recession or financial crisis short of a complete collapse of the US government’s ability to honor its deposit insurance obligations (an event with no historical precedent in the United States). The differences between credit unions and banks during recessions are real but nuanced: credit unions have historically had lower failure rates, but the deposit insurance covering both provides equivalent protection for insured balances at either institution type.

The Federal Insurance Backstop: The Foundation of Both Systems

The single most important fact in evaluating the safety of banks versus credit unions during recessions is that both types of institutions are covered by federal deposit insurance — and that federal deposit insurance has never failed to protect an insured depositor’s money since its creation in 1933 (FDIC) and 1970 (NCUA). Understanding how this insurance works is the foundation for everything else.

Banks are insured by the Federal Deposit Insurance Corporation (FDIC), an independent agency of the US government established in 1933 in response to the catastrophic bank failures of the Great Depression. The FDIC insures deposits up to $250,000 per depositor, per FDIC-insured bank, per ownership category. Ownership categories include: individual accounts, joint accounts, IRAs, trust accounts, and business accounts — each category is separately insured. A household with an individual checking account ($250,000), a joint savings account ($500,000 — the joint account limit is $250,000 per co-owner), and an IRA ($250,000) at the same bank has $1,000,000 fully insured under FDIC rules.

Credit unions are insured by the National Credit Union Administration (NCUA), an independent federal regulatory agency established in 1970. The NCUA operates the National Credit Union Share Insurance Fund (NCUSIF), which provides deposit coverage of $250,000 per member, per federally insured credit union, per ownership category — identical coverage structure and identical dollar limits to FDIC insurance. The NCUA also regulates approximately 4,700 federally chartered credit unions and the credit union system broadly.

Critically: both the FDIC and NCUA are backed by the full faith and credit of the United States government. In every bank failure and every credit union failure since deposit insurance was established, insured depositors have recovered 100% of their insured balances — without exception, without delay beyond normal processing time, and without political negotiation. This backstop is the bedrock of deposit safety in the US financial system.

Historical Failure Rates: Banks vs Credit Unions in Recessions

With the insurance backstop established as equivalent, the meaningful difference between banks and credit unions is their relative failure rates — how often each institution type actually fails, requiring the insurance to pay out. The historical record shows a consistent and significant difference.

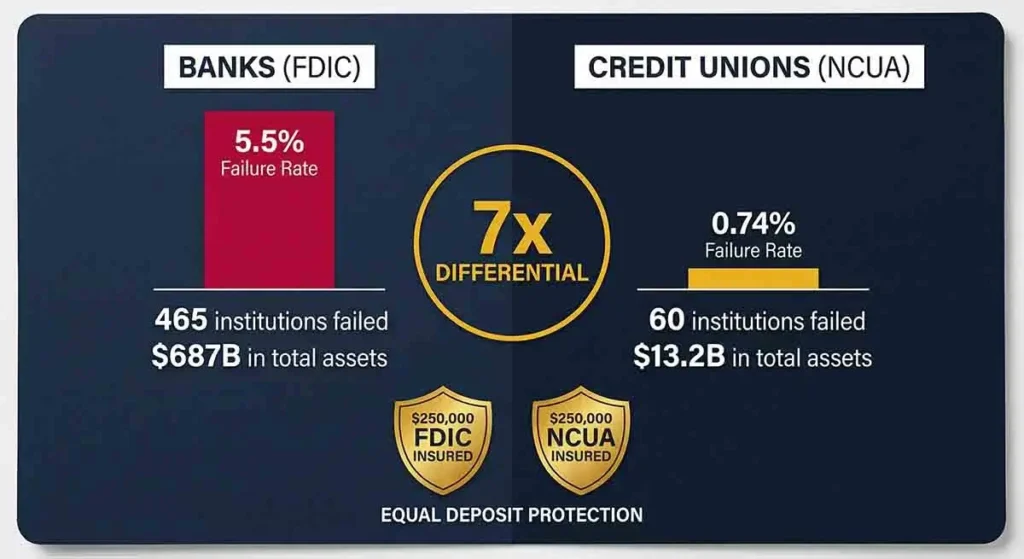

The 2008–2010 Financial Crisis: The Most Instructive Comparison

The 2008–2009 financial crisis produced the largest wave of US financial institution failures since the Great Depression — and provides the most instructive data point for comparing bank versus credit union resilience.

| Metric | Banks (FDIC-Insured) | Credit Unions (NCUA-Insured) |

|---|---|---|

| Total institutions (pre-crisis, 2007) | ~8,500 | ~8,100 |

| Failures 2008–2012 | 465 banks | ~60 credit unions |

| Failure rate | ~5.5% | ~0.74% |

| Total assets of failed institutions | $687 billion | $13.2 billion |

| Cost to insurance fund | $73 billion (FDIC) | $1.3 billion (NCUA) |

| Depositor losses above insured limits | None (insured balances) | None (insured balances) |

The failure rate difference is striking: approximately 5.5% of banks failed versus approximately 0.74% of credit unions — a 7x differential in failure rate during the worst financial crisis since the Depression. This difference reflects the structural differences between the two institution types discussed in detail below. However, crucially: insured depositors at every single failed bank and failed credit union during this period received 100% of their insured balances. The insurance worked exactly as designed at both institution types.

The 1980s Savings and Loan Crisis

The S&L crisis of the 1980s — during which approximately 1,000 savings and loan institutions (a type of bank-adjacent thrift institution) failed — is sometimes cited as a bank safety concern. However, the S&L crisis primarily affected savings and loan associations (S&Ls), not commercial banks or credit unions. Credit unions were largely unaffected by the S&L crisis, reflecting their different business model and member-ownership structure. The crisis ultimately cost taxpayers approximately $132 billion through the Federal Savings and Loan Insurance Corporation (FSLIC) — which was separate from the FDIC and was itself insolvent and required a taxpayer bailout.

COVID-19 Recession (2020): Minimal Institutional Stress

The 2020 COVID recession was severe but brief — and the combination of unprecedented fiscal stimulus (PPP loans, stimulus checks, enhanced unemployment), Federal Reserve emergency interventions, and regulatory forbearance (allowing loan modifications without automatic classification as defaults) prevented the wave of bank and credit union failures that typical recessions produce. Only 4 banks failed in 2020, and zero credit unions failed and were liquidated by the NCUA — an extraordinarily low failure rate reflecting the effectiveness of the policy response rather than any inherent institutional strength in such a sharp but brief downturn.

Why Credit Unions Have Lower Historical Failure Rates: The Structural Reasons

Credit unions’ better historical survival rate reflects several structural characteristics that make them inherently more conservative institutions:

Member-ownership and cooperative structure: Credit unions are owned by their members — each member has one vote regardless of account balance, and credit unions return profits to members through lower loan rates, higher deposit rates, and lower fees rather than distributing them to external shareholders. This cooperative structure aligns the institution’s interests with its members’ financial wellbeing in ways that pure profit-maximization logic does not. Credit unions have no external shareholders demanding quarterly earnings growth that can incentivize excessive risk-taking.

Field of membership restrictions: Credit unions are chartered to serve a specific “field of membership” — an employer, community, association, or other defined group. This restriction concentrates the institution’s member base in ways that both limit geographic diversification and create stronger community bonds and loyalty. Members who share an employer, community, or affiliation are more likely to maintain their accounts through stress rather than flee at the first sign of difficulty. The corollary limitation: field of membership restrictions mean credit union loan portfolios are also concentrated in their specific communities — a vulnerability if a specific industry or region experiences severe economic stress (as happened to some credit unions serving manufacturing-dependent communities in the Rust Belt).

Conservative lending culture: Credit unions historically maintain more conservative lending standards than commercial banks — lower loan-to-value ratios on mortgages, shorter loan terms, and stronger documentation requirements. This conservatism produces lower yields during economic expansions but significantly lower default rates during contractions. Credit union net charge-off rates (the percentage of loans written off as uncollectible) have been consistently lower than equivalent bank rates across multiple economic cycles.

Capital adequacy: Well-capitalized financial institutions are more resilient in downturns — their capital buffer absorbs losses before depositors are exposed. Credit unions’ net worth ratios (the credit union equivalent of capital adequacy) have generally been higher than comparable community bank ratios, providing an additional cushion during stress periods. “Well-capitalized” credit unions (net worth ratio above 7%) are the vast majority of the system — approximately 93% of insured credit unions are well-capitalized by NCUA standards.

Where Banks Have Advantages: The Objective Assessment

A fair analysis requires acknowledging the areas where banks provide safety or practical advantages over credit unions:

FDIC’s financial resources vs NCUA: The FDIC’s Deposit Insurance Fund has accumulated significantly larger resources than the NCUA’s Share Insurance Fund. As of 2025, the FDIC’s DIF holds approximately $125 billion — a reserve ratio of approximately 1.28% of insured deposits. The NCUA’s NCUSIF holds approximately $20 billion. In a systemic crisis requiring simultaneous payouts from both funds, the FDIC’s larger absolute size provides somewhat more buffer — though both funds have explicit access to the US Treasury as a backstop for truly systemic scenarios.

Larger banks = more diversification: The largest US commercial banks (JPMorgan Chase, Bank of America, Wells Fargo, Citibank) hold diversified portfolios across thousands of industries, hundreds of geographies, and dozens of product types — a diversification that makes simultaneous severe losses across the portfolio less likely than at a credit union serving a single employer or community. A credit union whose entire membership works for a single manufacturer faces catastrophic concentrated risk if that manufacturer declares bankruptcy.

TBTF (Too Big to Fail) implicit guarantee: During the 2008 financial crisis, the US government effectively guaranteed the largest banks’ survival through TARP (Troubled Asset Relief Program) and other extraordinary interventions — not because they were legally required to, but because systemic risk considerations made allowing these institutions to fail unacceptably dangerous. This “too big to fail” implicit backstop means that depositors at the largest US banks enjoy a de facto additional layer of protection that small community banks and credit unions do not have. This is an ethically controversial policy reality, but a practical safety consideration.

The Practical Safety Framework for 2026

Given everything above, here is the practical framework for evaluating the safety of your deposits at credit unions versus banks in 2026:

For balances below $250,000 at any institution: Federally insured banks and federally insured credit unions are equally safe. Your insured balance will be returned in full in any bank or credit union failure scenario — this is guaranteed by the federal government with no historical exceptions. The choice between a federally insured bank and a federally insured credit union for balances under $250,000 should be made entirely on practical factors: interest rates offered, fee structures, product availability, customer service quality, branch/ATM access, and technology platform quality.

For balances above $250,000: Diversification across multiple institutions (up to $250,000 at each) provides the strongest protection. This applies equally to banks and credit unions — the $250,000 per-institution limit applies at both. Using IntraFi’s CDARS or ICS programs (which spread large balances across multiple FDIC-insured banks while maintaining a single banking relationship) can efficiently manage large deposits above the single-institution limit.

For state-chartered credit unions without NCUA insurance: A small number of credit unions operate under state charters with private insurance rather than NCUA insurance. These institutions are not federally insured — verify insurance status before depositing. Any federally insured institution (bank or credit union) will display the FDIC or NCUA insurance logo. If you cannot verify federal insurance, do not deposit.

Choosing Between a Credit Union and Bank in 2026: The Real Factors

Since both institution types provide equivalent federal deposit protection for insured balances, the meaningful differences for most consumers relate to practical financial benefits rather than safety:

Credit unions typically offer: lower loan interest rates (auto loans, personal loans, and home equity products are consistently 0.5–1.5% lower at credit unions than comparable banks on average), higher deposit rates (credit unions’ return of profits to members produces deposit rates above commercial bank averages), lower fees (credit unions charge lower or zero fees for many services that commercial banks monetize significantly), and more relationship-based service (particularly for members experiencing financial difficulty — credit unions have historically shown more willingness to work with struggling members than commercial banks).

Banks typically offer: more extensive branch and ATM networks (particularly national banks with thousands of locations), more advanced digital banking technology (larger banks invest more heavily in mobile and online banking platforms), broader product availability (complex investment and wealth management products, business banking services, international banking), and more accessible membership (anyone can bank at a bank; credit union membership requires meeting field of membership criteria, though most Americans now qualify for at least one credit union through community charters or employer relationships).

The credit union membership search tool at MyCreditUnion.gov allows any American to find credit unions they are eligible to join based on their location, employer, and affiliations — most Americans qualify for multiple credit unions, including large ones with national footprints like Navy Federal, PenFed, and Alliant Credit Union that offer near-bank-level convenience.

💬 0 Comments