Millions of Americans receive some form of government check every month — Social Security payments, pension distributions, tax refunds, or disability benefits — and in 2026, predatory check-cashing services, high-fee prepaid cards, and payday lenders actively target this population. Understanding how to cash a check for free or near-free, and how to avoid the fees that quietly drain hundreds of dollars per year from check-dependent households, is genuinely valuable financial knowledge in a recession economy.

Check-cashing fees at payday lenders and retail check-cashing stores typically range from 1–5% of the check’s face value — meaning a $1,500 Social Security check costs $15–$75 to cash. Over 12 months, that is $180–$900 in fees on checks that can be cashed completely free through bank accounts, credit unions, or the US Treasury’s own Direct Express program. Never pay to cash a government check.

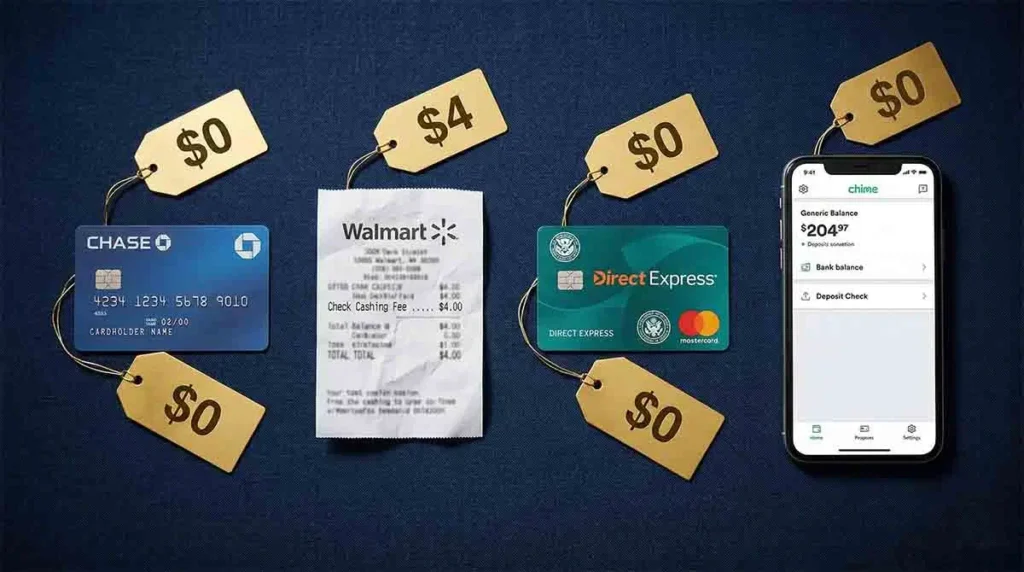

The Cheapest Ways to Cash a Check in 2026

Option 1: Your own bank or credit union account (free). If you have a checking or savings account at any bank or credit union, depositing and withdrawing from checks is free. Mobile check deposit (photographing the check through your bank’s app) makes this process entirely remote — no branch visit required. Funds from government checks (Social Security, tax refunds, government payroll) are typically available the next business day under Regulation CC rules; some banks make them available immediately for established customers.

Option 2: The issuing bank (free or low-fee). Most banks will cash a check drawn on their own account at no charge to the check recipient, even if you do not have an account there. A US Treasury check, for example, can be cashed at most banks for free or a minimal fee. Bring a government-issued photo ID. Some banks charge non-customers a fee of $5–$10 to cash a check not drawn on their institution — but this is still far less than a percentage-based check-cashing fee on a large check.

Option 3: Walmart Money Center (flat fee of $4 for checks up to $1,000; $8 for checks up to $5,000). For unbanked individuals, Walmart’s flat-fee check cashing is among the lowest-cost options available. The flat fee of $4 on a $1,500 check represents just 0.27% — dramatically better than the 1–3% charged by payday lenders and check-cashing stores. Walmart cashes payroll checks, government checks, tax refunds, cashier’s checks, and insurance settlement checks.

Option 4: Ingo Money app. Ingo Money allows you to photograph and cash checks through a mobile app, with funds deposited to a PayPal balance, a prepaid card, or a bank account. The fee structure: 1% for payroll and government checks (minimum $5), 4% for personal checks, or free with a 10-day processing delay. For government checks over $500, the 1% fee at Ingo compares favorably to check-cashing stores but unfavorably to the bank and Walmart options above.

The Direct Express Card: The Right Solution for the Unbanked Receiving Government Benefits

The US Treasury’s Direct Express® Mastercard Debit Card is specifically designed for Social Security, SSI, VA, and other federal benefit recipients who do not have bank accounts. Benefits are deposited directly to the card on payment day — no check required, no cashing fees, no waiting. The card is accepted anywhere Mastercard is accepted and can be used for purchases, bill payments, and ATM cash withdrawals.

Direct Express fee structure: no monthly fee, no direct deposit fee, one free ATM cash withdrawal per deposit per month (additional withdrawals cost $0.85 each), and no fee for balance inquiries at Direct Express network ATMs. For a Social Security recipient receiving one monthly deposit, the effective monthly cost is $0 for the primary free withdrawal. Compare this to $15–$75/month at a check-cashing store — the Direct Express card saves this population $180–$900/year.

Apply at GoDirect.gov or by calling 1-800-333-1795. There is no credit check to obtain a Direct Express card — it is available to any federal benefit recipient regardless of credit history or prior banking relationships.

Opening a Bank Account With No Credit Check: Second-Chance Banking

Many Americans who lack bank accounts have been denied by traditional banks due to negative entries in ChexSystems — a consumer reporting agency that tracks banking history (bounced checks, unpaid overdrafts, fraud). In 2026, several excellent banking options are available for people with ChexSystems issues:

Chime (chime.com): No credit check, no ChexSystems check, no monthly fee, no minimum balance. Includes a Visa debit card, mobile banking, and early direct deposit (funds available up to 2 days before the scheduled payment date). No overdraft fees for qualifying direct deposit customers. One of the most widely used second-chance banking solutions in 2026.

Current (current.com): No credit check, no monthly fee for the basic tier, early direct deposit, and fee-free overdraft protection up to $200 for qualifying accounts. Includes a spending analysis app and competitive savings pod features.

Credit union second-chance accounts: Many credit unions offer “fresh start” or “opportunity” checking accounts specifically for people who have been denied traditional accounts. These accounts typically have a monthly fee of $5–$10 that is eliminated after 12 months of responsible account management, after which you graduate to a standard account. The National Credit Union Administration’s credit union locator at ncua.gov helps you find credit unions in your area that serve your community.

Bank On certified accounts: The Cities for Financial Empowerment Fund certifies bank accounts that meet specific low-fee, accessible standards under the Bank On program. Bank On certified accounts have no minimum balance requirements, monthly fees under $5, no overdraft fees, and no ChexSystems requirement. Over 40,000 Bank On certified account locations exist across the US in 2026. Find certified accounts at joinbankon.org.

Prepaid Debit Cards: Understanding the Fee Traps

Prepaid debit cards are widely marketed to unbanked and underbanked Americans and are available at virtually every grocery store and pharmacy. They provide a payment mechanism without a bank account — but their fee structures are often predatory and opaque. Common fees on prepaid cards: monthly maintenance fees ($5–$10/month), reload fees ($3–$6 per cash reload), ATM withdrawal fees ($2–$3.50 per withdrawal), inactivity fees ($3–$7/month after 90 days of inactivity), balance inquiry fees ($0.50–$1 per inquiry), and in some cases, fees simply to check your balance by phone.

Before choosing any prepaid card, calculate the total annual cost of your expected usage pattern. A prepaid card with a $7.95/month maintenance fee, $3 per reload twice a month, and $2.50 per ATM withdrawal twice a month costs: $95.40 + $72 + $60 = $227.40/year in fees alone. The Chime or Bank On alternatives above provide equivalent functionality at zero or near-zero annual cost.

The best prepaid cards with lowest fees in 2026 if a prepaid card is truly necessary: the Bluebird by American Express (available at Walmart) with no monthly fee and free cash reloads at Walmart, and the Walmart MoneyCard which has a $5.94 monthly fee waived when you load $500+ per month.

Avoiding Payday Lenders: The Most Expensive Money in America

Payday loans — short-term loans typically for $200–$500 due on your next payday — carry effective annual percentage rates of 300–400% or higher. A $15 fee on a $100 two-week payday loan represents a 391% APR. In 2026, payday lending remains legal in 27 states, and approximately 12 million Americans use payday loans annually — paying approximately $9 billion in fees for access to short-term credit.

Every major alternative to a payday loan: a credit union Payday Alternative Loan (PAL) — federally regulated, maximum fee of $20, maximum APR of 28%, available to credit union members of 30+ days; a cash advance from a credit card (25–30% APR — expensive, but far less than 300%+); an employer payroll advance (many employers offer interest-free advances through earned wage access programs like DailyPay, PayActiv, and Earnin); a personal loan from an online lender (40–80% APR for poor credit — still far better than payday loan rates); or calling your landlord, utility company, or medical provider directly to arrange a payment plan — which is free.

💬 0 Comments