Annuities are among the most debated financial products in existence under any economic conditions — but during periods of recession risk, the debate intensifies. Insurance agents promoting annuities as “protected” from market volatility clash with financial advisors warning about high fees and surrender charges, while confused consumers try to determine whether their existing annuity or a newly proposed one will actually protect them during an economic downturn. This complete guide cuts through the confusion with a product-type-by-product-type analysis of how different annuities perform during recessions, grounded in historical data and the specific risk profile of each product structure.

The safety of an annuity during a recession depends entirely on which type of annuity you hold — and the types vary from genuinely recession-proof (fixed annuities from highly rated insurers) to potentially severe-recession-vulnerable (variable annuities with stock market exposure). The one risk that applies to all annuity types regardless of product structure is insurance company insolvency risk — which is mitigated by state guarantee associations but not eliminated. Understanding the specific risk profile of your annuity type is essential before concluding you are either safe or exposed.

Why Annuities Are Uniquely Affected by Recessions

Annuities are contracts with insurance companies — not bank deposits, not securities holdings. This legal structure means they interact with recessions through a different set of mechanisms than stocks, bonds, or savings accounts. Three primary recession risk channels affect annuities:

Insurance company financial health: Annuity guarantees are only as reliable as the insurance company behind them. During recessions, insurance companies face increased claims (life insurance death benefits, disability insurance claims), investment portfolio losses (their general account investments can decline), and potential surrender pressure (policyholders who need cash may attempt to surrender policies). A financially stressed or insolvent insurer may be unable to honor its annuity obligations — the most serious annuity risk in any recession scenario.

Investment account performance (for variable annuities): Variable annuities invest your premium in sub-accounts that function like mutual funds. These sub-accounts decline in value during market downturns — a recession that causes a 30–40% stock market decline produces equivalent losses in variable annuity sub-accounts, subject to any optional rider protections that may provide a floor.

Interest rate environment: Recessions typically produce falling interest rates as the Federal Reserve cuts to stimulate economic activity. Falling rates affect different annuity types differently: they increase the payout rates on newly-issued immediate annuities (counterintuitive — rates move inversely to payouts on some structures), reduce the returns available on newly-purchased fixed annuities, and affect the insurer’s ability to invest general account assets productively to support existing guarantees.

Fixed Annuities (Including MYGAs): Most Recession-Resistant

Fixed deferred annuities — including Multi-Year Guaranteed Annuities (MYGAs) — provide a guaranteed fixed interest rate for a specified term, completely independent of stock market performance. Your principal is contractually guaranteed, and the stated interest rate is contractually guaranteed, regardless of what happens in financial markets during the term. In 2026, MYGAs with 2–5 year terms are available at rates of 4.0–5.5% APY from highly rated insurers — competitive with or exceeding HYSA and CD rates, with the contractual guarantee of a fixed rate for the full term.

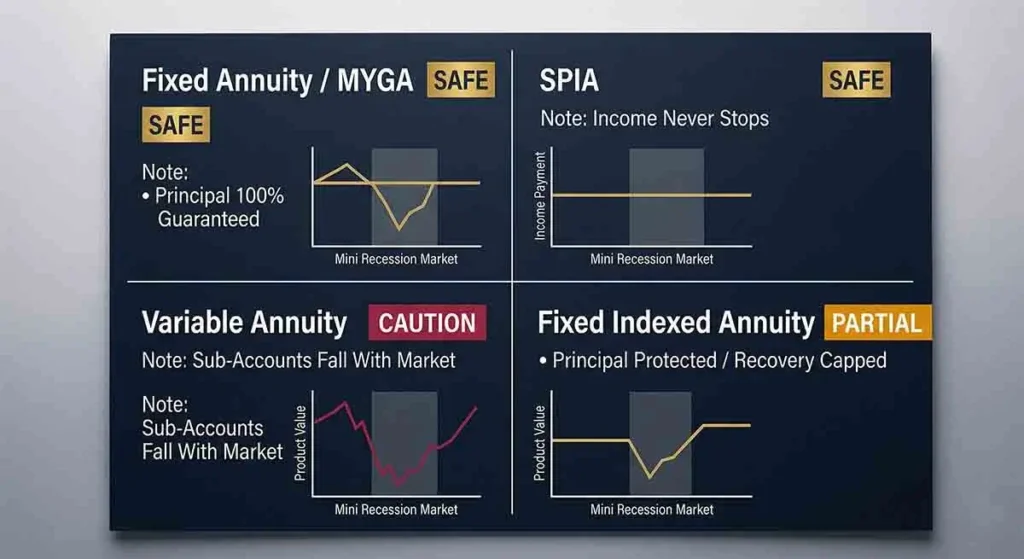

Recession safety assessment: Fixed annuities are as safe as the insurance company issuing them plus the state guarantee association backstop. They carry zero market risk — you will not lose principal due to stock market declines. They carry no liquidity risk within the surrender charge period (you can access your funds after the surrender period or by accepting the early withdrawal penalty). The primary risk is insurer insolvency — mitigated by investing only with A-rated or better carriers and confirming state guarantee association coverage for your policy amount.

Historical performance: Fixed annuities from solvent insurers have weathered every recession since their wide adoption in the mid-20th century without loss of principal or interest to policyholders. During the 2008–2009 financial crisis — the most severe test of insurer resilience in modern history — even the failures that occurred (Executive Life, Confederation Life in an earlier period) were managed through state guarantee associations and regulatory rehabilitation without loss to policyholders within the guarantee limits in most cases.

Immediate Annuities (SPIAs): Truly Recession-Proof Income

Single Premium Immediate Annuities (SPIAs) convert a lump sum into a stream of guaranteed lifetime income payments that begin immediately. Once the SPIA is purchased and income payments begin, the insurer is contractually obligated to make those payments for the policyholder’s lifetime — regardless of market conditions, interest rate movements, or general economic conditions. The payments are fixed in nominal terms (not inflation-adjusted unless a cost-of-living adjustment rider was purchased) and backed by the insurer’s general account assets and state guarantee associations.

Recession safety assessment: SPIA income payments are among the most recession-resistant income sources available to retirees. Unlike dividend income (which companies can cut), rental income (which tenants may default on), or portfolio withdrawal income (which depletes faster in down markets), SPIA income payments do not vary with economic conditions. A 70-year-old who purchased a SPIA in 2007 — at the peak of the market, just before the financial crisis — continued receiving identical monthly income payments throughout the 2008–2009 crash, the recovery, and every subsequent period. The payments never missed. The payments never declined. This recession resilience is precisely the longevity insurance value proposition of SPIAs.

The insolvency risk caveat: SPIA income depends on the insurer remaining solvent. During the 2008 crisis, a small number of insurers (primarily those with significant exposure to commercial real estate and structured credit products) experienced severe stress. State guarantee associations — each state operates one that provides a backstop for insurance policies issued by insolvent insurers — protect SPIA income up to state-specific limits, typically $250,000 in present value of annuity benefits. Spreading large SPIA purchases across multiple highly-rated insurers provides additional protection above the guarantee association limits.

Variable Annuities: Recession-Vulnerable Without Riders

Variable annuities are the most complex and most contested annuity product — and the type most commonly sold inappropriately to consumers who do not understand their recession vulnerability. A basic variable annuity (without optional living benefit riders) invests your premium in sub-accounts that function like mutual funds — your account value rises and falls with the performance of those underlying investments. There is no guarantee of your principal or of any specific account value.

Recession safety assessment (without riders): A variable annuity sub-account invested in equity funds during a recession loses value in proportion to the equity market decline — a 35% market decline produces approximately a 35% variable annuity account value decline, minus the annuity’s annual fees (typically 2.5–4.0% per year in mortality and expense charges, administrative fees, and sub-account expenses). The fee structure means that variable annuities typically underperform equivalent mutual fund investments by the full fee amount annually — creating a compounding disadvantage that is most damaging during market downturns when every dollar of preserved value is most critical.

Recession safety assessment (with GLWB riders): Many variable annuities are sold with Guaranteed Living Withdrawal Benefit (GLWB) riders that provide a guaranteed minimum withdrawal rate (typically 4–6% per year) on a “benefit base” even if the account value declines to zero. This rider provides recession protection — a guaranteed income floor even if the underlying sub-accounts decline severely. The protection comes at significant cost: GLWB riders typically add 0.75–1.25% in annual fees, bringing total variable annuity costs to 3.0–5.0% per year. This cost substantially reduces the net return relative to the guaranteed income protection provided.

The practical question for variable annuity holders during a recession: how valuable is your GLWB guarantee given its cost? A policyholder with a $200,000 benefit base and a 5% GLWB guarantee has secured $10,000/year in lifetime income regardless of market performance — a potentially valuable floor that justified the rider cost if the account value has declined significantly. A policyholder whose account value still significantly exceeds the benefit base may be paying for protection they have not needed.

Fixed Indexed Annuities (FIAs): Partial Recession Protection

Fixed Indexed Annuities link returns to the performance of a market index (typically the S&P 500) up to a cap rate or participation rate, with a floor (typically 0%) protecting against market losses. The floor — which prevents loss of principal due to index declines — provides genuine recession protection: a year where the S&P 500 falls 25% produces zero credit in an FIA (the floor kicks in) rather than a 25% account value decline.

Recession safety assessment: FIAs protect principal from market declines — a meaningful advantage over variable annuities without riders during recessions. During 2008–2009, FIA holders saw their account values “floor” at zero crediting for the down years rather than declining with the equity market — a genuine protection benefit that the products correctly advertise. However, FIAs carry their own recession risks: the “cap” and “participation rate” limits on upside capture the post-recession recovery incompletely (if the cap is 8% and the S&P 500 recovers 30% in 2009, the FIA credits only 8%), and the insurer’s ability to honor the floor guarantee depends on its financial health during the recession.

The primary FIA concern is not recession safety per se — it is that the combination of complex terms, high agent commissions (7–10% of premium), and performance limitations that reduce the recovery capture means FIAs often deliver poor long-run returns despite their recession protection marketing. An FIA that floors losses during the recession may credit 6–8% annualized during the recovery while a diversified index fund recovers 15–20% annualized — capturing the downside protection at the cost of significantly reduced upside.

The Insurance Company Solvency Question: How to Evaluate Your Insurer’s Strength

All annuity types — fixed, SPIA, variable, indexed — ultimately depend on the insurer’s ability to honor its obligations. Evaluating insurer financial strength before purchasing or holding an annuity is essential financial due diligence that most consumers skip. The primary financial strength rating services for insurance companies:

AM Best (ambest.com) is the most insurance-specialized rating agency. AM Best’s financial strength ratings range from A++ (Superior) through D (Poor). For annuity safety in a recession scenario, limit purchases to insurers rated A (Excellent) or better by AM Best — specifically A, A+, or A++. Some of the highest-rated life insurers as of 2026: New York Life (A++), Northwestern Mutual (A++), TIAA (A++), Pacific Life (A+), and MassMutual (A++). These insurers have maintained top ratings through multiple economic cycles including 2008.

Moody’s, S&P, and Fitch also rate insurance company financial strength. Look for Aa3/AA- ratings or above from these agencies for equivalent confidence.

State guarantee associations provide a backstop for insolvent insurer claims, but the coverage limits (typically $250,000 in present value of annuity benefits, varying by state) mean large annuity contracts may have uninsured exposure above those limits. The Life and Health Insurance Guarantee Association (NOLHGA at nolhga.com) provides a state-by-state directory of guarantee associations and their specific coverage limits.

Practical Guidance: What Annuity Holders Should Do in 2026

For existing annuity holders: review your insurer’s current AM Best rating — any downgrade below A should prompt consultation with a fee-only fiduciary financial advisor about whether repositioning is appropriate. Review your specific contract’s surrender schedule — if you are past the surrender period or approaching its end, your options for repositioning are significantly better. If you hold a variable annuity with a GLWB rider that has been activated (account value near or below the benefit base), the income guarantee may be the most valuable component of the contract — potentially more valuable than surrendering for the current account value.

For prospective annuity buyers in 2026: fixed annuities (MYGAs) from A-rated insurers represent genuinely recession-safe savings vehicles for money you will not need within the surrender period, paying 4.5–5.5% with full principal guarantee. SPIAs from highly-rated insurers represent genuinely recession-proof income for money you want to convert to guaranteed lifetime income. Variable annuities without riders and FIAs with high fees and complex terms should be evaluated very carefully by a fee-only advisor before purchase — the recession marketing often oversimplifies the product’s actual risk-return profile.

The essential rule for 2026: before purchasing any annuity, get a second opinion from a fee-only fiduciary financial advisor (one who earns no commission on the products they recommend) who can evaluate the specific contract against your complete financial situation. The complexity of annuity products makes unbiased second opinions particularly valuable — and the commission structure of annuity sales (among the highest in the financial services industry) makes the potential conflict of interest in the initial recommendation particularly significant.

💬 0 Comments