Your credit score is one of the most consequential three-digit numbers in your financial life — it determines the interest rate on your mortgage, whether you can rent an apartment, what you pay for car insurance, and in some industries, whether you get a job offer. Yet most Americans have only a vague understanding of what constitutes a “good” credit score, how the scoring system works, and what specific steps move the needle most effectively. This complete guide clarifies all of it.

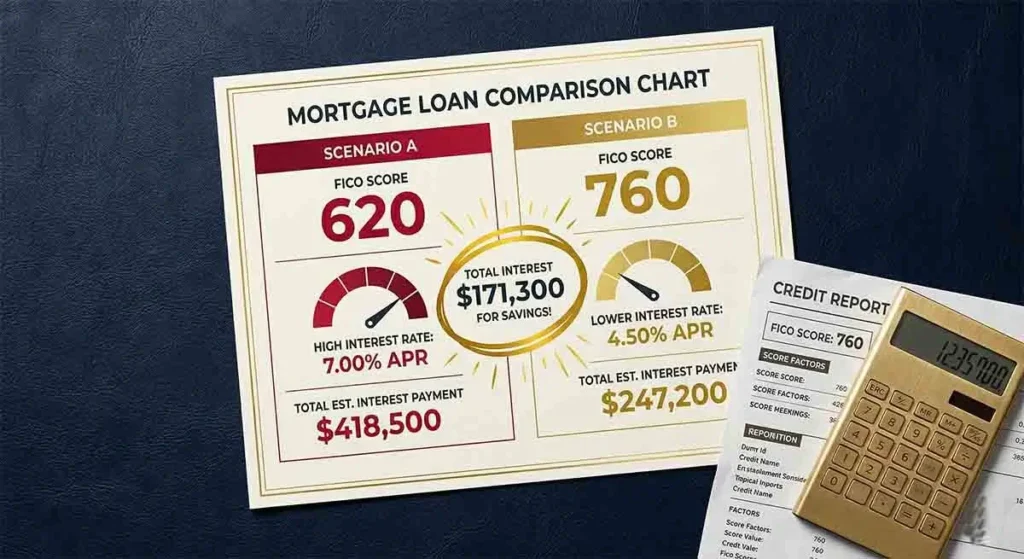

A FICO score of 670 or above is considered “good” — qualifying you for most credit products at competitive rates. A score of 740+ is “very good” and unlocks the best mortgage rates and premium credit cards. A score of 800+ is “exceptional” and represents the top tier of creditworthiness. The difference between a 620 and a 760 FICO score on a $350,000 30-year mortgage costs approximately $68,000 in additional interest over the life of the loan — making your credit score one of the most financially valuable numbers in your life to optimize.

The Complete FICO Score Range: What Every Tier Means

| FICO Score Range | Rating | % of Americans | What You Qualify For |

|---|---|---|---|

| 800–850 | Exceptional | ~23% | Best rates on all products; premium cards with highest rewards; lowest insurance premiums |

| 740–799 | Very Good | ~25% | Excellent mortgage rates; most premium credit cards; favorable auto loan rates |

| 670–739 | Good | ~21% | Most credit products at competitive rates; standard mortgage qualification |

| 580–669 | Fair | ~17% | Some credit products at higher rates; FHA mortgage may be available; higher auto loan rates |

| 300–579 | Poor | ~16% | Limited credit access; secured cards required; deposits required for utilities; rental difficulty |

The Real Dollar Cost of a Low Credit Score

Abstract score ranges become concrete when you calculate what they cost in actual dollars. Here is the interest rate and payment difference across credit score tiers on two common loan types in 2026:

| FICO Score | 30-Year Mortgage Rate (est.) | Monthly Payment ($350K loan) | Total Interest Paid |

|---|---|---|---|

| 760–850 | 6.50% | $2,213 | $446,680 |

| 700–759 | 6.72% | $2,264 | $464,870 |

| 680–699 | 6.85% | $2,294 | $475,840 |

| 660–679 | 7.08% | $2,347 | $495,020 |

| 640–659 | 7.50% | $2,447 | $531,160 |

| 620–639 | 8.08% | $2,594 | $584,120 |

The difference between a 760 score and a 620 score on this mortgage: $381/month and $137,440 in total interest. This is not a marginal distinction — it is the equivalent of years of additional mortgage payments. For auto loans, the spread is similarly dramatic: a 36-month auto loan on a $30,000 vehicle ranges from approximately 5.5% APR (excellent credit) to 15–20% APR (poor credit) — a difference of $150–$250/month on the same car.

The Five FICO Factors: What Builds and Destroys Your Score

Payment History (35% of score): The single most important factor. A single 30-day late payment can drop a good score by 60–110 points — and stays on your credit report for 7 years. The remedy: set up autopay for at least the minimum payment on every account. You can always pay more manually — but autopay ensures you never miss a due date due to forgetfulness. If you have a late payment, its impact diminishes over time — a late payment from 4 years ago has less impact than one from 6 months ago.

Credit Utilization (30% of score): The percentage of your available revolving credit you are currently using. Utilization is calculated both per-card and in aggregate. The commonly cited 30% rule is a floor, not a target — the highest scorers keep utilization below 10%. A $5,000 balance on a card with a $6,000 limit (83% utilization) damages your score severely. The same $5,000 balance on a card with a $50,000 limit (10% utilization) has minimal impact. Request credit limit increases proactively — higher limits reduce utilization without requiring you to reduce spending.

Length of Credit History (15% of score): The age of your oldest account, your newest account, and the average age of all accounts. Never close your oldest credit card — even if you no longer use it. The annual fee cost of keeping an old card open is zero (if it has no fee) versus the score cost of closing it. If an old card has an annual fee, call and request a product change to a no-fee version of the same card — which maintains the account age without the cost.

Credit Mix (10% of score): Having both revolving credit (credit cards) and installment credit (auto loans, mortgages, personal loans, student loans) demonstrates you can manage different credit types responsibly. You do not need to take on debt specifically to improve your credit mix — but if you already have installment loans, ensuring they are managed well contributes positively to this factor.

New Credit Inquiries (10% of score): Each hard inquiry (when a lender checks your credit for a new application) temporarily reduces your score by 5–10 points and remains on your report for 2 years. Multiple mortgage or auto loan inquiries within a 14–45 day window (depending on the FICO version) typically count as a single inquiry — allowing you to rate-shop without multiple score impacts. Space out new credit applications by at least 6 months wherever possible.

The Fastest Legitimate Ways to Improve Your Credit Score in 2026

Pay down revolving balances to below 10% utilization: This is the fastest single action that moves your score. Utilization is recalculated every time your credit card issuer reports to the bureaus (typically monthly, aligned with your statement date). Paying down a $4,000 balance on a card with a $5,000 limit to $400 can improve your score by 40–80 points within one billing cycle — faster than any other single action.

Dispute errors on your credit report: Approximately 25% of Americans have at least one material error on their credit report according to the FTC. Get free reports from all three bureaus at AnnualCreditReport.com and review every account for accuracy. Dispute errors at each bureau’s online portal — errors must be investigated within 30 days under the Fair Credit Reporting Act.

Request a credit limit increase: Many card issuers allow you to request a credit limit increase through their mobile app or website without a hard inquiry (a “soft pull” review). Increasing your limit reduces your utilization ratio immediately. On a card with a $5,000 limit and a $2,000 balance (40% utilization), a limit increase to $10,000 drops utilization to 20% — improving your score within the next billing cycle.

Become an authorized user on a well-managed account: As discussed in our credit-building guide, being added as an authorized user on an account with long history, low utilization, and perfect payment record can add positive history to your file — useful for both building and rebuilding credit.

Experian Boost: Free tool that adds on-time utility, phone, and streaming service payments to your Experian credit file. Average score increase: approximately 13 points for thin-file consumers. Takes 5 minutes at experian.com/boost.

Credit Score Myths That Cost People Money

Myth: Checking your own credit hurts your score. Checking your own credit is a “soft inquiry” and has zero impact on your score. Only hard inquiries (from lenders you apply to) affect your score. Check your score as frequently as you like — it is essential monitoring, not damage.

Myth: Carrying a balance builds credit faster. There is no benefit to carrying a credit card balance (and paying interest) versus paying in full each month. Your payment history is what matters — not whether you carry a balance. Paying your statement balance in full every month builds excellent credit and costs you zero in interest.

Myth: Closing old cards improves your score. Closing a credit card reduces your total available credit (increasing utilization) and eventually reduces your average account age — both negative effects. Keep old cards open with a small recurring charge and autopay. The only valid reason to close a card is if its annual fee exceeds the value you receive from it — and even then, request a product change rather than closure if possible.

Myth: Paying off a collection account removes it from your report. Under standard credit bureau rules, paid collections remain on your credit report for 7 years from the original delinquency date — though the major bureaus voluntarily removed paid medical collections in 2022. For non-medical paid collections, the negative mark remains — though it typically has less impact on your score after 2 years and especially after 4 years.

Where to Check Your Score for Free in 2026

Multiple legitimate free score options exist in 2026. Your credit card issuer likely provides a free FICO score — Discover, Capital One, Chase, Citi, American Express, and many other issuers provide free monthly FICO scores through their apps. Credit Karma provides free VantageScore 3.0 scores from Equifax and TransUnion weekly. Experian.com provides free monthly FICO Score 8 (the most widely used FICO version) with a free Experian account. AnnualCreditReport.com provides free credit reports (but not scores) from all three bureaus — the reports are what you need for accuracy verification.

💬 0 Comments