Something unusual is happening in the American labor market in 2026 — and most people with jobs are not aware of it, because from where they stand, everything looks fine. Unemployment is at 4.3%. Layoffs have not surged. The economy added 178,000 jobs in March. By the headline numbers, the labor market looks more like a soft landing than a crisis.

But for the more than seven million Americans who are unemployed and actively searching for work, the experience is completely different. A new phrase has entered the economic vocabulary to describe what they are facing: the job seeker recession. As reported, these workers are facing a job market that, by every hiring measure, looks like a recession — while the broader unemployment numbers that capture their distress remain contained enough that official recession declarations remain distant.

“More than seven million unemployed Americans are facing a job market that, by hiring measures, looks like a recession,” according to our analysis. “Meanwhile layoffs and unemployment are relatively low, creating a split labor market that is stable for people who have jobs, and recession-like for those trying to find one. This combination of slow hiring and low unemployment is unprecedented in more than 25 years of government data.”

This cornerstone guide examines every dimension of this unprecedented labor market split: what the job seeker recession actually is, why it differs from a traditional labor market downturn, the rolling recession dynamic that produced it sector by sector, the hard data behind the hiring collapse, who is being hurt most severely, the Iran war energy shock that threatens to convert the slow-motion hiring recession into a full economic contraction, and the most evidence-based strategies for job seekers navigating the most difficult placement environment in a generation.

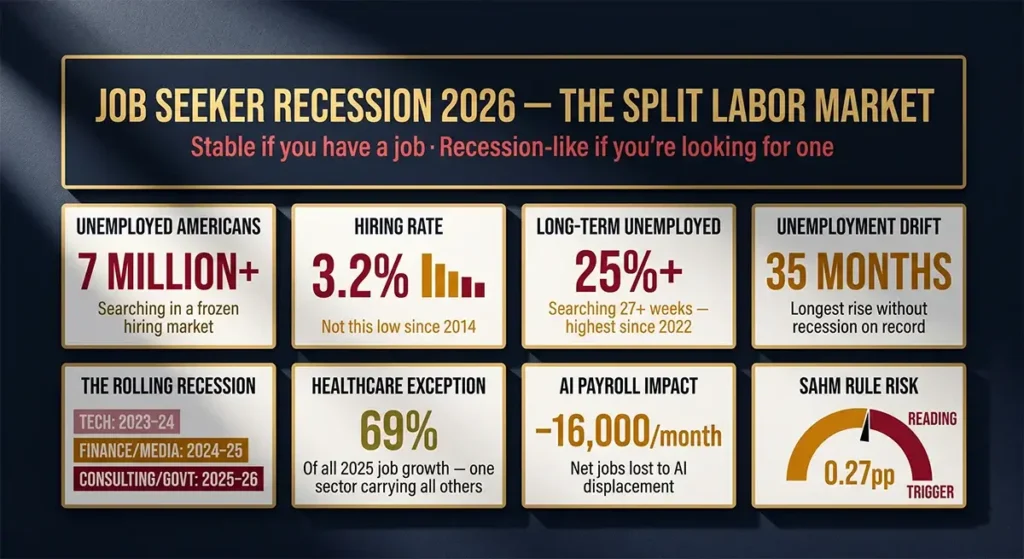

The US labor market in 2026 is experiencing a historically unprecedented split: unemployment at 4.3% masks a hiring rate that has collapsed to levels not seen since 2014, over 25% of unemployed workers searching for 27+ weeks (long-term unemployment at a 4-year high), and a job-to-applicant ratio that has reversed from the 2022 peak of nearly 2 openings per unemployed worker to near parity. This is the job seeker recession — a labor market that is stable for the employed and recession-like for those seeking work. The Iran war energy shock, with Goldman Sachs projecting unemployment rising to 4.6% by Q3 2026, now threatens to convert the hiring recession into a broader economic recession before the hiring environment has had time to recover.

What Is a Job Seeker Recession? Defining the 2026 Labor Market Split

The term “job seeker recession” describes a specific and historically unusual labor market configuration that has no exact precedent in the modern data record. In a conventional recession, two things typically happen simultaneously: employers lay off workers at elevated rates, and they stop hiring. Both unemployment rises and hiring falls. The signal is unambiguous because the forces operate in the same direction.

The 2026 labor market is doing something different. The layoff component of the conventional recession signal is largely absent — employers are not firing workers at elevated rates, and the unemployment rate’s rise from its 3.4% trough in April 2023 to 4.3% in March 2026 has been driven primarily by labor supply normalization (immigration slowdown, labor force participation changes) rather than mass employer-initiated separations. But the hiring component has collapsed to recession-equivalent levels without the matching surge in firing that would make it visible in the headline unemployment rate.

According to the Bureau of Labor Statistics JOLTS (Job Openings and Labor Turnover Survey), the hiring rate fell to 3.2% in November 2025 — one of the lowest rates since 2013, when the labor market was still rebuilding from the Great Recession. ZipRecruiter labor economist Nicole Bachaud noted that the hires level had not been this low since 2014 outside of the 2020 pandemic year. The Indeed Hiring Lab confirmed that the Indeed Job Postings Index had returned to near pre-pandemic levels after the extraordinary 2021–2022 surge, with the structural shift visible in virtually every sector outside healthcare.

The most telling statistic defining the job seeker recession is the long-term unemployment share. As of December 2025, 26% of all unemployed workers had been out of work for at least six months — the highest share since February 2022 and a steep increase from approximately 18% three years prior. Over 25% of unemployed Americans had been searching for at least 27 weeks as of early 2026. This is the arithmetic signature of a hiring freeze: not more people becoming unemployed, but the same people staying unemployed for much longer because the doors that would normally lead them back to work are closed.

Fortune captured the psychological dimension: “Job prospects during the pandemic were grim. After all, companies shuttered their windows, business went online, and recessionary forces put most hiring on ice. Of course, most job hunters at the time felt as though the job market was frozen solid.” In 2026, workers are reporting that the job market feels similar to pandemic conditions — even though the macro numbers suggest something far less severe. The gap between the lived experience of job seekers and the reported headline indicators is the defining characteristic of the job seeker recession.

The Rolling Recession: How the Labor Market Slowdown Spread Sector by Sector

The labor market slowdown of 2025–2026 did not arrive in the way that conventional recessions do — as a simultaneous, across-the-board contraction visible in every sector at once. Instead, it spread as a rolling recession: a sequential deterioration that moved through different sectors at different times, always present somewhere in the economy but never fully visible in the aggregate because sectors still expanding in one period masked sectors already contracting in another.

The rolling recession concept was developed by economists to describe periods when the economic pain is real and severe for those experiencing it but distributed unevenly enough across time and sector that the aggregate indicators remain positive. It is a recession that is always happening somewhere — just not everywhere simultaneously — and its victims find little policy sympathy because the headline numbers suggest the overall economy is fine.

Phase 1: Technology Sector (2023–2024)

The rolling recession’s first major wave hit the technology sector in 2023, following the extraordinary overhiring of 2020–2022. Meta, Google, Amazon, Microsoft, Salesforce, and hundreds of smaller technology firms had hired aggressively in anticipation of sustained digital acceleration that ultimately moderated. The correction began in late 2022 and intensified through 2023: approximately 245,000 tech workers were laid off in 2025 alone, according to layoffs.fyi, following even larger waves in 2023 and 2024. Technology workers who had never experienced job insecurity faced suddenly frozen hiring markets, resume review queues counted in thousands per position, and six-to-twelve-month searches that would have been unimaginable at the peak of the 2021–2022 market.

The technology rolling recession produced the first cohort of long-term unemployed knowledge workers in the modern data record — highly credentialed, well-compensated workers experiencing the specific conditions that the job seeker recession describes: low layoff rates at a portfolio level (most tech workers were not being laid off) but collapsed hiring rates making re-entry after displacement extraordinarily difficult.

Phase 2: Financial Services, Media, and Professional Services (2024–2025)

The second wave of the rolling recession moved into financial services, media, and professional services through 2024 and 2025. Banking sector headcount reductions — driven by a combination of AI automation of compliance and analysis functions, interest rate margin compression, and merger consolidation — produced significant displacement in roles that had historically been reliable ports of entry and advancement for college graduates. Media sector contraction accelerated as AI content generation tools reduced the headcount required for standard-format content at scale.

This second wave expanded the job seeker recession’s demographic footprint. The technology wave had primarily affected software engineers, product managers, and technical program managers — workers with skills that, while suddenly in lower demand, remained valuable and transferable. The financial services and media wave hit a broader range of educational profiles, including entry-level and mid-career workers whose skills were less differentiated and whose re-employment options were more constrained.

Phase 3: Consulting, Government, and General Corporate (2025–2026)

The third wave — the one producing the specific conditions described as the job seeker recession in April 2026 — has spread into consulting, government contractors, and general corporate functions. The DOGE workforce reduction eliminated approximately 182,528 federal workers through early 2026, creating a sudden large cohort of former government employees entering a private-sector labor market that was not expanding rapidly enough to absorb them. Major consulting firms including Booz Allen Hamilton, McKinsey, and Deloitte had reduced headcount across practice areas. The specific anecdote that emerged captures the sector breadth of this third wave: Aaron Laniewicz, in his 40s, left his consulting position at Booz Allen Hamilton in August 2025 and had withdrawn approximately $50,000 from his retirement savings to manage debt while searching. Robin Peppers Daniel, a former Wells Fargo vice president in her 60s, had been searching since April 2025 and was working as a substitute teacher after months without placement.

Healthcare, notably, has been insulated from all three waves — adding 76,000 jobs in the March 2026 report and accounting for approximately 69% of all job growth across 2025. The sector split between a booming healthcare labor market and a frozen market everywhere else is one of the clearest structural features of the rolling recession: the economy is not uniformly weak, it is specifically weak in the sectors where the most workers are displaced and specifically strong in a sector where the supply of qualified workers (requiring specific credentials and training) cannot be rapidly expanded by the displaced workers from frozen sectors.

The Hard Data: Understanding the Scale of the Hiring Collapse

The job seeker recession is best understood through a set of data points that collectively paint a picture that the headline unemployment rate obscures:

Unemployment drift duration — 35 months without recession: According to the Indeed Hiring Lab’s analysis, US unemployment has risen from its 3.4% trough in April 2023 to 4.3% in March 2026 — a 35-month upward drift that represents the longest sustained deterioration in the unemployment rate on record without a recession following. Every prior episode in which unemployment rose from a low base but remained below 4.5% was eventually followed by a recession, making the current episode genuinely unprecedented in its gradualism.

Hiring rate at decade-plus lows: The BLS JOLTS hiring rate of 3.2% (November 2025) represents one of the lowest monthly rates since 2013. The hires level had not been this low outside of 2020’s pandemic shock since the labor market was still recovering from the 2008–09 Great Recession. This is not a modest cooling — it is a hiring environment that, by the most direct measure of employer willingness to bring on new workers, is operating at crisis-equivalent levels.

25%+ long-term unemployment share: As of March 2026, over 25% of unemployed Americans had been searching for at least 27 weeks. Three years prior, that figure was approximately 18%. The 7-percentage-point increase in the long-term unemployment share represents a structural shift in the experience of unemployment: it is increasingly a state of prolonged exclusion rather than a brief transitional period between jobs.

AI’s marginal but growing payroll impact: Goldman Sachs research found that AI’s substitution effect on the labor market had reduced monthly payroll growth by approximately 25,000, while AI’s augmentation effect (using AI to enhance existing workers’ output) had added approximately 9,000 — for a net reduction of approximately 16,000 payroll jobs per month attributable to AI adoption. This is not yet the dominant driver of labor market weakness, but it represents an additional headwind that operates continuously and is likely to intensify as AI capabilities expand.

Job seekers worse off than during pandemic: Perhaps the most striking data point: workers report that their confidence in finding a job if laid off is now lower than during the pandemic in some surveys. The Federal Reserve Bank of New York’s Survey of Consumer Expectations found that in March 2026, the perceived probability of losing one’s job climbed to 14.4%, and the share of respondents expecting unemployment to be higher a year from now increased to 43.5% — the highest since April 2025. The gap between hiring availability and the number of people seeking work has created subjective labor market conditions that feel worse, to those experiencing them, than the acute crisis of 2020.

The “Low Hire, Low Fire” Labor Market: Why the Headline Numbers Mislead

The central analytical challenge of the 2026 labor market — and the reason the job seeker recession is not visible in the macro indicators that policymakers and media focus on — is the “low hire, low fire” equilibrium that employers have settled into for the past eighteen months.

In a traditional labor market, job turnover is high: workers quit voluntarily to take better positions (creating job openings), employers hire to fill vacancies and to grow, and the constant circulation of workers through the labor market means that someone displaced from one job typically finds another relatively quickly. The 2021–2022 labor market operated at the extreme version of this model: record quit rates (“The Great Resignation”), record job openings (11+ million), record hiring rates, and extremely short unemployment durations.

The 2025–2026 labor market has settled into the mirror image. Quit rates have declined sharply — workers who have jobs are not leaving them voluntarily, because they sense that finding equivalent alternatives has become difficult. Employers, facing uncertainty from tariffs, AI investment decisions, energy costs, and interest rates, have adopted what economists have called “labor hoarding”: maintaining existing headcount rather than laying off, but also strictly limiting new hiring. As CNBC noted in January 2026, “employers have been in a holding pattern for more than a year in a low-hire, low-fire environment that has kept unemployment contained but also struggled to add new positions despite solid economic growth.”

The practical consequence: the economy’s self-healing mechanism for the displaced has been disabled. In a high-turnover market, a laid-off worker competes primarily against other recent job-seekers, many of whom are voluntarily between positions and not urgently seeking. In a low-turnover market, the laid-off worker competes against every other unemployed person in their field — and there are many, because workers are staying in their current roles rather than creating vacancies. The competition per available opening has intensified dramatically even as the aggregate unemployment rate looks unremarkable.

The Iran War Threat: Converting the Hiring Recession Into a Full Recession

The labor market slowdown described above was already in place before the Iran war began on February 28, 2026. What the Strait of Hormuz closure has introduced is a new and potentially decisive headwind that threatens to convert the job seeker recession into a conventional recession — with the simultaneous rise in both layoffs and unemployment that would make the labor market’s pain visible even in the headline indicators.

Goldman Sachs has projected unemployment rising to 4.6% by Q3 2026 as the Iran war energy shock works through the economy. From the current 4.3%, a 0.3 percentage point increase would push the Sahm Rule reading materially closer to — and possibly through — the 0.50 trigger threshold that has preceded every US recession since 1960. Heather Long, Chief Economist at Navy Federal Credit Union, said following the March jobs report: “It’s likely to be a tough spring for job seekers.” Bankrate’s survey of economists found that 79% think unemployment will increase in the year ahead, with the average forecast calling for 4.5% unemployment by December 2026.

The sectors most immediately threatened by an Iran war-driven economic deterioration are precisely the ones that have thus far maintained employment stability during the rolling recession: transportation and logistics (directly affected by diesel at $5.45/gallon), manufacturing (energy cost pressure on production margins), consumer discretionary (household spending power squeezed by $4+ gasoline), and the services sector more broadly as the consumer confidence collapse drives spending deferrals. Healthcare — the sole sector that has carried the labor market through the rolling recession — would be the last to be affected, but even healthcare is not immune to an economic contraction that reduces consumer spending on elective procedures and suppresses the state and employer-provided insurance revenues that fund hospital systems.

The IMF’s April 2026 World Economic Outlook noted that in its severe scenario, “a number of countries would be in outright recessions” — and even in its adverse scenario, global growth falls to 2.5%, a level consistent with multiple advanced economies stalling. For American job seekers who have been navigating the job seeker recession for months or years already, the transition from a slow-hiring environment to an actively-contracting one would be catastrophic — arriving at the worst possible moment, when savings are depleted, mental health reserves are strained, and financial buffers have been drawn down through the extended search.

Who Is the Job Seeker Recession Hitting Hardest? The Four Most Vulnerable Groups

The job seeker recession is not evenly distributed. Four groups are experiencing its effects most acutely, and the overlap between these groups — workers who belong to more than one vulnerable category — defines the highest-distress population in the 2026 labor market.

Group 1: Mid-Career White-Collar Workers (Ages 40–60)

The anecdotes from the reporting — a Wells Fargo VP in her 60s working as a substitute teacher, a Booz Allen consultant in his 40s withdrawing retirement savings — are representative of a broader pattern. Mid-career white-collar workers in their 40s and 50s face a specific combination of vulnerabilities: their salaries at prior roles are high enough that employers with available openings often screen them out as overqualified or as creating compensation compression risks; their skills, while genuinely valuable, may be in categories that AI tools are specifically targeting (management coordination, report synthesis, client communication); and their networks, while extensive, were built in sectors now in contraction. Their longer-term unemployment duration also means their financial buffers are eroding precisely as the pressure of the search intensifies.

Group 2: Recent College and Graduate School Graduates

The collapse of entry-level hiring has created an acute placement crisis for 2024 and 2025 graduates who expected to enter labor markets that resembled the ones their slightly older peers had navigated in 2021–2022. Goldman Sachs research found that AI’s net negative payroll impact of 16,000 jobs per month falls “mainly affecting less experienced workers” — because AI tools are most capable of automating the entry-level tasks (research synthesis, report drafting, basic data analysis, customer support) that have historically served as the entry point into white-collar careers. PARWCC’s labor market outlook noted that “employers now expect clearer direction, stronger portfolios, and demonstrable skills — even for junior roles,” raising the effective entry bar to levels that graduating students have had no opportunity to meet through professional experience.

Group 3: Former Government and Government-Contractor Workers

The DOGE-driven federal workforce reduction — approximately 182,528 federal workers laid off through early 2026 — created a sudden large cohort of workers entering a private-sector labor market that was not structured to absorb them. Federal workers, whose careers have been defined by public-sector operational frameworks, security clearances, and government procurement specialties, often find their skills less directly transferable to private-sector roles than their resumes might suggest. Federal government salaries for many professional roles were already below private-sector equivalents, making downward salary adjustment a painful reality for many former federal workers seeking re-entry.

Group 4: Workers in “AI-Adjacent” Roles

The fourth vulnerable group — and potentially the largest over a five-to-ten-year horizon — consists of workers in roles whose core functions AI tools can demonstrably perform: content writers, marketing coordinators, data entry analysts, basic software testers, technical writers, customer service representatives, and the category that has shown the most acute displacement, technical program managers and project managers whose primary function is information coordination and synthesis across teams. These workers are finding that the hiring market for their specific role category has not merely slowed — it has structurally contracted, with employers explicitly citing AI tool adoption as the reason positions are not being backfilled when vacated.

The Policy Gap: Why Job Seekers Are Getting Less Help Than in Prior Recessions

One of the most practically consequential features of the job seeker recession is explicitly identified: “barring a wider economic downturn, a new round of expanded benefits is unlikely, particularly with a divided Congress and concerns about the level of government spending.” This represents a structural gap between the scale of labor market distress being experienced and the policy support being deployed.

In prior labor market downturns, government intervention was calibrated to the headline unemployment rate and the NBER recession declaration — both of which trigger political and institutional action. During the pandemic, federal lawmakers added $600/week to state unemployment checks and extended eligibility to 99 weeks. During the Great Recession, extended unemployment benefits covered workers for periods that reflected the genuine length of their searches. In the job seeker recession of 2025–2026, neither the headline unemployment rate (4.3% — unremarkable) nor the NBER declaration (not issued — no official recession) has triggered either mechanism. Job seekers are receiving standard state unemployment benefits — which cap at levels like North Carolina’s $350/week maximum — for standard eligibility periods, while experiencing search durations that reflect something far closer to recession-era conditions.

The practical consequence is a growing cohort of workers — like the Booz Allen consultant who withdrew $50,000 from retirement savings — who are self-financing searches that exceed the duration that state unemployment systems are designed to support. The financial damage of long-term unemployment is being absorbed directly by households rather than distributed through government support mechanisms, producing a kind of silent austerity that does not appear in any official economic indicator but represents real and persistent economic harm.

What the Best-Positioned Job Seekers Are Doing Differently

For the seven million Americans currently navigating the job seeker recession, the evidence — both quantitative and anecdotal — points to a specific set of strategies that separate those who achieve placement from those experiencing the extended searches that define the current environment.

Healthcare and AI-adjacent skill development as sector pivots: The structural concentration of job growth in healthcare creates a genuine re-entry pathway for workers from contracted sectors who are willing to invest in credential acquisition. Healthcare administration, medical billing, health information technology, and healthcare data analytics all represent roles that require genuine healthcare knowledge while drawing on skills (data management, process coordination, technology implementation) that workers from technology, financial services, and consulting sectors genuinely possess. The investment required — often 6 to 18 months of credentialing — is significant, but so is the hiring volume advantage of re-entering through the one sector that has consistently added jobs throughout the rolling recession.

AI fluency as the core differentiating credential: PwC research has found a 56% wage premium for workers who demonstrate effective AI tool proficiency within their specific domain. In a job market where employers are scrutinizing every hire more carefully than at any point since the Great Recession, the ability to demonstrate that you can do the work of 1.5 to 2 conventional workers by effectively leveraging AI tools is both a hiring differentiator and an earnings multiplier. This applies across sectors — not just technology. Healthcare professionals who demonstrate clinical AI tool proficiency, financial analysts who use AI for research acceleration, and marketing professionals who integrate AI content tools into campaign production are all showing the specific productivity evidence that hiring managers in a low-volume hiring environment most need to see.

Network activation over application-tracking system reliance: Robert Half’s March 2026 labor market update noted that “networking is always going to be one of your best friends” — and the data on how jobs are filled in the current environment makes this more true than ever. In a low-hiring environment, employers are more likely to fill the limited positions they do open through internal referrals and trusted network connections than through broad external posting. The job that appears on LinkedIn is often posted primarily for compliance or HR process reasons, with an internal candidate or referred hire already identified. Active cultivation of professional relationships — through alumni networks, industry associations, direct outreach to former colleagues in growing sectors — provides access to the unlisted positions and pre-competitive referrals that represent the most efficient path through the current market.

Financial runway extension as the strategic priority: The single most consequential variable determining job seeker outcomes in the current environment is financial runway — the number of months the searcher can sustain living expenses without forced employment decisions. Workers who are financially pressured accept the first adequate offer rather than the right offer; workers with runway can execute a deliberate, targeted search that matches their skills to the best available opportunities. In the job seeker recession, where optimal placement genuinely requires six to twelve months for many profiles, the difference between a three-month financial runway and a twelve-month one is the difference between a career-consistent placement and a survival-mode position that may be difficult to recover from.

Specifically: maximizing state unemployment benefits by filing immediately on the first day of displacement (not after severance expires), reducing discretionary spending to extend the period those benefits cover, and protecting retirement savings as the genuinely last-resort buffer (not a first-response mechanism, as the Booz Allen consultant’s experience illustrates) represent the financial management framework for navigating the job seeker recession with career trajectory intact.

What to Watch: The Key Indicators That Will Tell You If the Job Seeker Recession Is Getting Worse

For job seekers and their families monitoring the labor market trajectory, a small set of indicators provides the most accurate real-time signal of whether conditions are improving, stable, or deteriorating.

Initial jobless claims (weekly, every Thursday): The US Department of Labor’s weekly initial claims release is the most timely available indicator of employer-initiated layoff acceleration. The current trend of approximately 238,000/week is above the 200,000–210,000 range of early 2026 — the direction matters more than the level. A sustained move above 250,000 would signal that the low-layoff component of the “low hire, low fire” equilibrium is breaking down and transitioning toward conventional recession labor market dynamics.

JOLTS hiring rate (monthly, with 5-week lag): The BLS JOLTS report’s hiring rate — currently at multi-decade lows around 3.2% — is the most direct measure of the job seeker recession’s persistence. Any improvement above 3.5% sustained for two or more months would represent a genuine loosening of the hiring environment and a meaningful improvement in placement prospects. Deterioration below 3.0% would signal further intensification of the job seeker recession toward conditions not seen since 2013 outside of pandemic months.

Long-term unemployment share: The BLS monthly unemployment report includes the share of unemployed workers who have been searching for 27+ weeks. The current level of 25–26% is the single most direct measure of job seeker distress. Its direction — rising toward 30%+ would indicate severe structural deterioration; declining toward 20% would indicate labor market thaw — is the most consequential indicator for the seven million workers currently experiencing the job seeker recession.

The Sahm Rule reading: Currently at 0.27pp against a 0.50 trigger, the Sahm Rule will fire if Goldman’s 4.6% unemployment projection for Q3 2026 materializes. A trigger would signal that the job seeker recession has transitioned from a structural hiring-side phenomenon to a conventional demand-side recession — meaning that the workers who currently have jobs would begin joining the seven million who are searching, fundamentally changing the dynamics and difficulty of the current environment.

💬 0 Comments