In early 2025, a Chinese AI startup called DeepSeek released a large language model that reportedly matched the performance of America’s most advanced AI systems — trained at a cost of approximately $5.6 million, a fraction of the billions being spent by US competitors. In a single day, Nvidia lost $588.8 billion in market capitalization — the largest single-day market value destruction for any company in recorded financial history. Stocks recovered within weeks. The AI infrastructure buildout accelerated. Spending projections were revised upward. And the word “bubble” appeared with increasing frequency in the research notes of the world’s most respected financial institutions.

As of April 2026, the debate over whether the AI investment cycle constitutes a genuine financial bubble is not abstract or academic. It is the most consequential economic question in the global financial system — because the answer determines whether trillions of dollars of capital currently flowing into AI infrastructure represents the foundation of a genuine productivity transformation or one of the largest misallocations of capital in modern economic history. This cornerstone guide assembles every critical piece of evidence on both sides of the argument, grounded in the latest data from Goldman Sachs, JP Morgan, the Federal Reserve, MIT, Man Group, and the National Bureau of Economic Research.

The AI bubble debate in 2026 is uniquely complex because both the bulls and bears are partially right. The technology is genuinely transformative and the major infrastructure investors (Amazon, Microsoft, Google, Meta) are funding their buildout primarily from operating cash flows rather than borrowed money — unlike the leveraged speculation of the dot-com era. But the revenue gap is real, the circular financing structure is real, the 95% enterprise ROI failure rate documented by MIT is real, and the 10:1 ratio between AI capex ($660–690 billion) and direct AI revenue ($51 billion) in 2026 is structurally unsustainable at any historical precedent. The honest answer: not a bubble exactly like 1999 — but carrying specific risks that could produce significant financial disruption in the 2026–2028 period.

Defining the AI Bubble: What We Are Actually Talking About

A financial bubble exists when asset prices significantly exceed their intrinsic value based on fundamentals — driven by speculative expectation of future gains rather than current earning power. The classic bubble has several defining characteristics: rapid price appreciation driven by narrative rather than earnings, concentration of capital in a narrow asset class, leverage that amplifies both gains and losses, circular investment dynamics where investment returns depend on continued investment rather than external demand, and ultimate forced reckoning when expectations cannot be sustained by actual revenue.

The AI investment cycle of 2023–2026 exhibits some but not all of these characteristics — which is precisely what makes the debate so complex and why both the “clear bubble” and “definitely not a bubble” camps are oversimplifying a genuinely nuanced situation. Applying the bubble definition systematically to the current AI investment environment:

Rapid price appreciation driven by narrative: Confirmed. The S&P 500’s AI-adjacent component traded at 23 times forward earnings in late 2025 — the most stretched valuation since the dot-com era. The five largest US technology companies held 30% of the entire S&P 500 index, the highest concentration in half a century. Nvidia reached a $4.3 trillion market capitalization by February 2026, making it the world’s most valuable company with a price-to-earnings ratio of approximately 47× before the market correction. OpenAI carried a private valuation of $730 billion against $13 billion in revenue — a price-to-revenue multiple that would make most dot-com era investors blush.

Capital concentration in a narrow asset class: Confirmed. According to the Wall Street Journal, AI-related investment accounts for approximately half of US GDP growth. Goldman Sachs estimates AI capex reached $527 billion for 2026 — representing approximately 0.8% of GDP, approaching (though not yet at) the 1.5% of GDP reached during comparable technology investment booms of the past 150 years. The five hyperscalers (Amazon, Alphabet, Microsoft, Meta, Oracle) collectively planned to spend approximately $660–690 billion in AI capital expenditure in 2026.

Leverage: Partially confirmed, concentrated in specific nodes. Unlike the dot-com era — when technology companies were spending 4 times their free cash flow on capital investment — most hyperscalers are funding AI buildout primarily from operating cash flows. Fidelity’s analysis found capex-to-free-cash-flow ratios below 1× for the broad technology sector in 2026, compared to 4× at the dot-com peak. However, specific companies present extreme leverage: Oracle took on $58 billion in new debt in two months to fund AI commitments. OpenAI projects $14 billion in losses by end of 2026 despite $20 billion in revenue, funded by continuous capital raising. Morgan Stanley estimates global data center spending of $3 trillion between 2025 and 2028, half of which is covered by private credit.

Circular investment dynamics: Confirmed — and the most alarming structural feature of the current cycle. Man Group’s research paper “The AI Bubble: Hidden Risks and Opportunities” (2026) identified a “closed, recursive financing loop” among hyperscalers: rising valuations justify heavier capex; rising capex signals explosive future demand; the signal itself reinforces valuations. As Man Group’s analysts noted: “Revenue growth can appear spectacular because each node in the loop pays another. Capex looks justified because demand from inside the loop appears endless. But the demand signal becomes circular and divorced from the market.” This circular dynamic is the defining structural risk of the current AI cycle that has no direct equivalent in the dot-com era analysis.

The Revenue Gap: The Number That Cannot Be Ignored

The most powerful single data point in the AI bubble debate is the spending-to-revenue gap. In 2026, hyperscalers collectively deploy approximately $660–690 billion in AI-specific capital expenditure. Direct AI revenue generated by those investments is approximately $51 billion. That is a spending-to-revenue ratio of approximately 10:1.

For context: when cloud computing was at the equivalent stage of its adoption curve in 2011, the capex-to-revenue ratio was approximately 2.4:1. The current AI ratio is more than four times more extreme than cloud computing’s investment phase — and cloud computing’s investment phase was itself considered aggressive at the time. The Wall Street Journal has reported that American consumers spend only approximately $12 billion per year on AI services directly. Derek Thompson, writing in The Atlantic in 2025, described the economic gap as the difference between Singapore’s GDP (AI infrastructure investment) and Somalia’s GDP (actual AI consumer revenue) — a chasm between the vision and the current commercial reality.

The NBER study published in February 2026 provided the most damning enterprise data point in the debate: 90% of firms reported no measurable impact of AI on workplace productivity — yet those same executives projected AI would increase productivity by 1.4% and output by 0.8% in the future. This is the definition of the productivity paradox — investment preceding productivity, belief preceding evidence. MIT’s research, cited in the Wikipedia AI Bubble article, found that despite $30–40 billion in enterprise investment in generative AI, “95% of organizations are getting zero return.” The gap between investment and measured return is not a temporary delay — it is, after two full years of widespread enterprise AI deployment, a structural feature of the current adoption cycle that should inform any honest assessment of bubble risk.

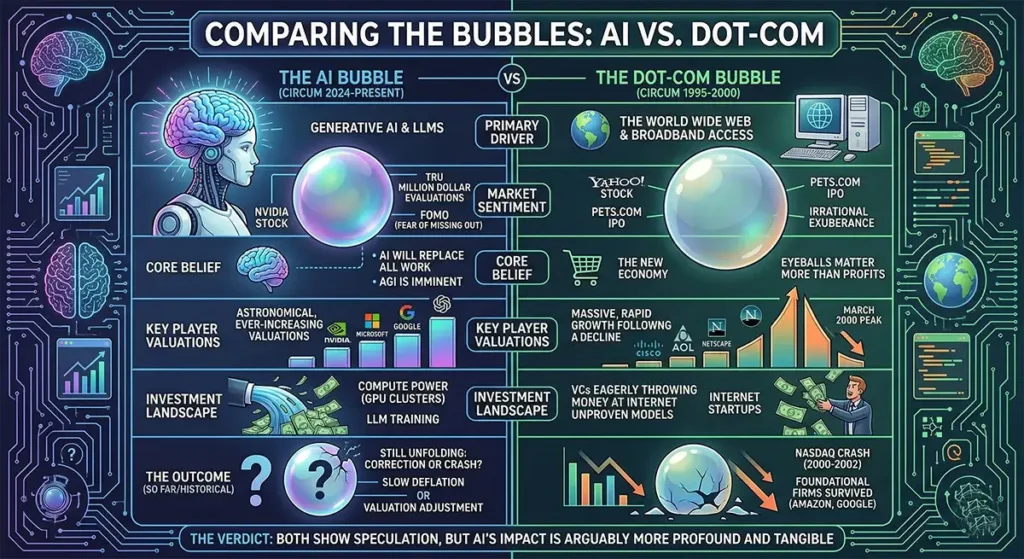

The AI Bubble vs the Dot-Com Bubble: The Critical Comparison

The most frequently cited historical analogy for the AI bubble is the dot-com bubble of 1995–2000 — and the comparison is both instructive and imperfect. Understanding both the similarities and the differences is essential for assessing the actual risk.

| Characteristic | Dot-Com Bubble (1999–2000) | AI Bubble (2024–2026) |

|---|---|---|

| Primary asset valuation driver | Pure narrative — most companies had zero revenue | Narrative + real earnings — Nvidia, Google, Microsoft have massive profits |

| Investment funding source | Primarily debt and equity raises by unprofitable companies | Mix — hyperscalers from cash flow, AI labs from equity/debt |

| Capex-to-free-cash-flow ratio | ~4× at peak (spending 4x what was earned) | ~0.9× for broad tech sector; specific companies much higher |

| Market concentration | Top 5 companies = ~18% of S&P 500 | Top 5 companies = ~30% of S&P 500 — historically unprecedented |

| Revenue-to-investment gap | Extreme — most dot-com companies had no revenue model | Significant — $51B revenue vs $660B+ capex = 10:1 ratio |

| Circular financing | Present but less documented | Explicitly documented by Man Group, Yale, and multiple analysts |

| Leverage in system | High — widespread debt-funded speculation | Moderate for hyperscalers; extreme for Oracle, AI labs |

| Potential crash magnitude | Nasdaq fell 78% peak to trough | Most estimates suggest 30–60% correction in AI stocks; systemic risk lower |

Federal Reserve Chair Jerome Powell has explicitly distinguished the current environment from the dot-com bubble, pointing to the substantial realized revenue of major AI companies and characterizing AI infrastructure spending as a “major engine of broader economic growth.” Fidelity’s February 2026 analysis similarly found that current technology companies are largely spending within their means rather than borrowing against future promises as dot-com companies did. Ray Dalio of Bridgewater Associates disagreed, saying in early 2025 that investment levels are “very similar” to the dot-com bubble. Jamie Dimon of JP Morgan said in October 2025 that he believes “some money invested now will be wasted” and that “the level of uncertainty should be higher in most people’s minds.”

The most nuanced analysis comes from Capital Economics’ chief markets economist John Higgins, who told Fortune in late March 2026 that the AI stock bubble has already partially burst — but that a more dangerous “fundamental bubble” in AI earnings themselves may still be inflating. “Normally we think of a bubble as being something where the price has gotten out of whack with the fundamentals themselves,” Higgins said. “In this case, the bubble actually may be in the earnings themselves.” If AI company earnings are themselves inflated by the circular financing loop — where hyperscalers pay each other for services that are internally funded by continued capital raising — then even current valuations that look reasonable relative to current earnings may be built on a foundation that could erode when the capital cycle tightens.

The Three Ways the AI Bubble Could Burst

Yale School of Management’s Jeffrey Sonnenfeld identified three distinct scenarios through which an AI financial correction could materialize, each with different severity and transmission mechanisms.

Scenario 1 — The Chain Reaction (2008-Style): The interconnected ownership structure of major AI companies creates systemic concentration risk with no historical parallel. As Sonnenfeld documented: OpenAI is taking a 10% stake in AMD, while Nvidia is investing $100 billion in OpenAI; OpenAI also counts Microsoft as a major shareholder; Microsoft is a major customer of CoreWeave; Nvidia holds a significant equity stake in CoreWeave; and Microsoft accounted for nearly 20% of Nvidia’s revenue. This recursive ownership web means that a significant disappointment at any one node — an OpenAI product failure, a CoreWeave insolvency, a Microsoft earnings miss on AI-related revenue — could cascade through the system in ways that resemble the 2008 structured credit contagion rather than the relatively contained dot-com collapse. Goldman Sachs CEO David Solomon said he expects “a lot of capital that was deployed that doesn’t deliver returns.” Amazon founder Jeff Bezos called the current environment “kind of an industrial bubble.”

Scenario 2 — The Technology Obsolescence Shock (Fiber Optic Scenario): The DeepSeek shock of January 2025 was a preview of this risk. A breakthrough in semiconductor chip efficiency, quantum computing, or AI model architecture could render the current $700 billion data center buildout partially or wholly obsolete — as fiber optic cable infrastructure built during the dot-com era sat largely unused for years after the bubble burst. Bethany McLean’s Washington Post analysis noted the parallel explicitly: the 1990s fiber buildout was rendered unnecessary by a “technological breakthrough that made each line exponentially more powerful, multiplying existing capacity.” If DeepSeek-style efficiency gains continue to compress the compute required for state-of-the-art AI performance, the economic justification for $660 billion in annual data center investment could erode faster than the infrastructure can be monetized.

Scenario 3 — The Revenue Disappointment (Gradual Deflation): The most probable scenario — not a dramatic crash but a prolonged period of multiple compression as AI revenue growth fails to materialize at the pace required to justify current capital expenditure levels. The 2026 earnings season for major technology companies — specifically whether AI capex is generating proportional AI revenue growth — will be the first major test of this scenario. If Q1 and Q2 2026 earnings reveal continued widening of the capex-to-revenue gap, institutional investors who have been patient may begin rotating out of AI-exposed positions, triggering a self-reinforcing decline in valuations and tightening of the capital markets that AI companies depend on for continued funding.

The Case That This Is Not a Bubble: The Bull Arguments

A thorough analysis requires taking the bull case seriously rather than dismissing it. The arguments that the AI investment cycle will prove justified are substantive.

Nvidia’s earnings validate the infrastructure thesis: Nvidia’s fiscal year 2026 revenue reached $215.9 billion — up 65% year-over-year — with Q4 revenue of $68.1 billion and net profit margins of approximately 53%. A company with these financial results is not a speculative vehicle; it is one of the most profitable hardware companies in history. The demand for its products from hyperscalers who are generating their own massive cash flows represents genuine commercial activity, not circular financial engineering at the fundamental level.

The productivity gains are beginning to appear: Erik Brynjolfsson, writing in the Financial Times in early 2026, argued that AI productivity gains are now measurable in US economic data. Studies consistently show performance gains of 10–25% in knowledge tasks — writing, research, programming, and financial analysis — among workers using AI tools actively. The WEF found 86% of employers expect AI to transform their business by 2030 and 85% are prioritizing internal upskilling. PwC’s research documented a 56% wage premium for workers using AI effectively. These are not zero-return signals — they are the early indicators of a productivity transformation that typically takes a decade to fully materialize in aggregate economic statistics.

The capex-to-cash-flow ratio does not indicate speculative excess: Fidelity’s analysis found that the broad technology sector’s capex-to-free-cash-flow ratio remained below 1× in early 2026 — meaning companies were spending within their means, not borrowing against speculative futures. This is the single most structurally important difference from the dot-com era, where the equivalent ratio hit 4×. The hyperscalers can absorb a 30–40% correction in AI valuations without existential financial stress, unlike the leveraged dot-com companies that collapsed entirely when equity markets closed.

AI agents represent genuine new demand: 2026 is being called “the year of AI agents” — autonomous AI systems that can execute complex multi-step tasks over extended periods. Claude Code and competing agentic systems represent a qualitative leap beyond chatbots that could dramatically expand computing demand per user. If agent adoption materializes at scale, the current infrastructure buildout may prove to have been appropriately sized for a demand wave that has not yet arrived.

The Depreciation Time Bomb: The Risk Most Investors Are Ignoring

The most underappreciated risk in the AI investment cycle — identified by Michael Burry (who predicted the 2008 housing crisis) and documented in detail by TechConstant’s analysis — is the depreciation mismatch. The five largest hyperscalers currently depreciate AI servers over five to six years, assuming the hardware will generate economic value throughout that period. Burry argues the real useful life of current AI chips, given the pace of architectural improvement, is two to three years.

If Burry is correct, the industry is understating its depreciation by an estimated $176 billion between 2026 and 2028 — roughly equivalent to the entire annual revenue of a major technology company. When this depreciation hits balance sheets — either through accelerated write-downs forced by auditors as hardware utility declines, or through the simple arithmetic of forced hardware replacement cycles — the profitability picture for AI infrastructure companies changes dramatically. Bank of America estimates the hyperscalers are pushing capex to 94% of operating cash flow in 2026, up from 76% in 2024. These companies can absorb significant financial stress — but the depreciation reckoning, when it comes, will not be invisible.

What the AI Bubble Debate Means for Your Investments and Financial Planning

For individual investors navigating the AI investment landscape in 2026, the bubble debate has direct practical implications. The specific guidance of respected institutional investors converges on several themes.

Avoid companies dependent on continuous capital market access for AI strategy execution: Cresset Capital’s 2026 analysis explicitly named this as the primary risk management criterion. Companies like OpenAI (which projects $14 billion in losses by end of 2026), CoreWeave (whose entire business model depends on GPU demand remaining insatiable), and Oracle (which has staked its transformation on a $300 billion deal with a company that has never been profitable) are most vulnerable if capital markets tighten. Oracle’s credit default swap spread spiked to approximately 180 basis points in late 2025 — roughly equivalent to the sovereign credit risk of Romania — reflecting exactly this concern about debt-funded AI ambitions.

The most vulnerable AI stocks are not Nvidia: Capital Economics’ Higgins and multiple institutional analysts identify the highest AI bubble risk in AI application companies and neocloud infrastructure providers rather than in the semiconductor companies with genuine earnings. The companies that monetize the infrastructure buildout phase — the picks-and-shovels plays like Nvidia — are financially substantiated in ways that the companies dependent on AI generating enterprise ROI at scale are not. A 95% enterprise zero-ROI finding from MIT suggests the application layer is where bubble valuations are most exposed.

The 2026 earnings season is the critical inflection point: Q1 and Q2 2026 earnings reports from major technology companies — specifically the relationship between AI capital expenditure and AI-attributable revenue growth — will provide the clearest signal yet of whether the revenue gap is closing or widening. Microsoft’s ability to demonstrate “Copilot” revenue surge, Amazon Web Services’ AI contribution to cloud revenue growth, and Google’s AI-driven revenue diversification will be scrutinized more intensely in 2026 than in any prior year. If these reports show the gap narrowing, the bull case strengthens substantially. If they show it widening, the correction scenario Scenario 3 described above begins to accelerate.

Diversification away from AI concentration is rational regardless of bubble outcome: Whether the AI investment cycle ultimately validates or collapses, the unprecedented market concentration — 30% of the S&P 500 in five companies — represents structural risk that is independent of the bubble question. A portfolio that reduces this concentration through broader diversification into sectors with lower AI exposure improves resilience under multiple scenarios, including the gradual deflation scenario that does not require a dramatic crash to produce meaningful wealth erosion in AI-heavy portfolios.

The Milestones That Will Answer the Question in 2026 and 2027

Several specific events in 2026 and 2027 will provide empirical evidence that significantly resolves the bubble debate either way. Monitor these closely:

Q1 and Q2 2026 AI earnings season: The revenue-to-capex relationship in major technology company earnings will be the most important data set in the bubble debate. Specifically: Microsoft’s AI-attributable revenue growth relative to its $35 billion quarterly AI capex, Google Cloud AI revenue contribution, and Amazon Web Services AI service adoption rates. Sustained widening of the gap is a bubble confirmation signal; sustained narrowing is a bull validation signal.

Enterprise ROI assessments entering year 3: Many enterprises began significant generative AI deployments in 2023–2024. By 2026–2027, these companies have 2–3 years of implementation data and will be making go/no-go decisions about continued AI platform investment. If enterprise pilot failure rates persist at the 90–95% zero-ROI level documented by MIT, enterprise spending on AI applications will disappoint projections and the application layer of AI investing will face significant pressure. Positive enterprise ROI data, conversely, would validate the productivity narrative.

Potential IPOs of OpenAI and Anthropic in late 2026: The public market pricing of these two flagship AI labs will serve as a critical valuation test. OpenAI at $730 billion private valuation against $13 billion in revenue and a path to $14 billion in losses by year-end represents the sharpest private-market bubble test in the current cycle. If these IPOs proceed at or above current private valuations, the bull case for AI valuations broadly is strengthened. If they are withdrawn or priced dramatically below private valuations, it signals a significant repricing of AI risk at the institutional level.

💬 0 Comments