Before the war in Iran began on February 28, 2026, the UK economy was already limping. GDP growth had slowed to just 0.1% in each of Q3 and Q4 2025. Business investment was falling. Consumer confidence remained historically weak. The Bank of England had barely begun cutting interest rates before the energy shock forced it to stop. The Office for Budget Responsibility was forecasting only 1.1% growth for the full year — itself a subdued number that most independent forecasters considered optimistic. Then the Strait of Hormuz closed, oil crossed $100 per barrel, and Britain found itself at the epicenter of what the OECD would describe as the most severe economic hit to any developed-market nation from the Iran war.

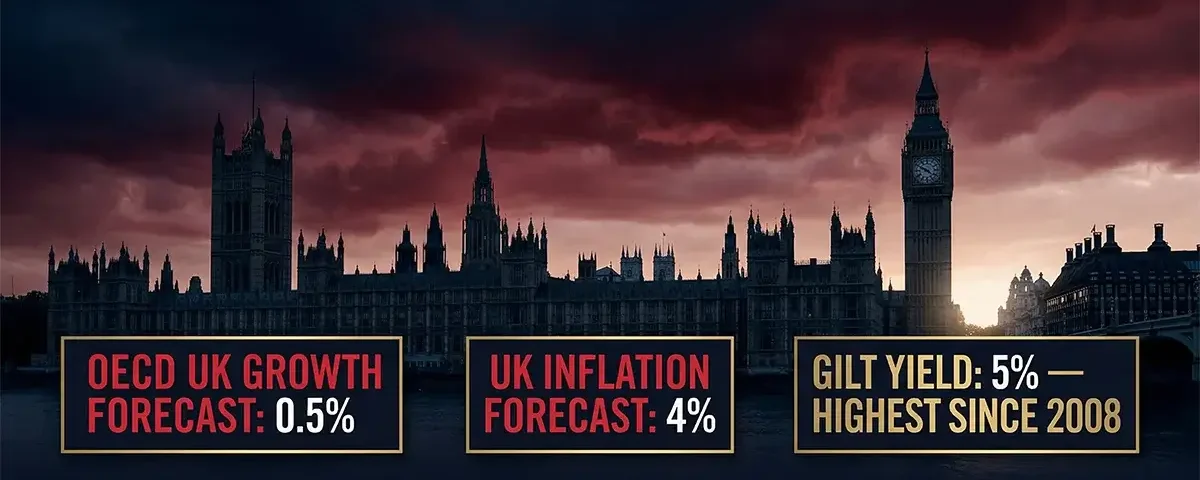

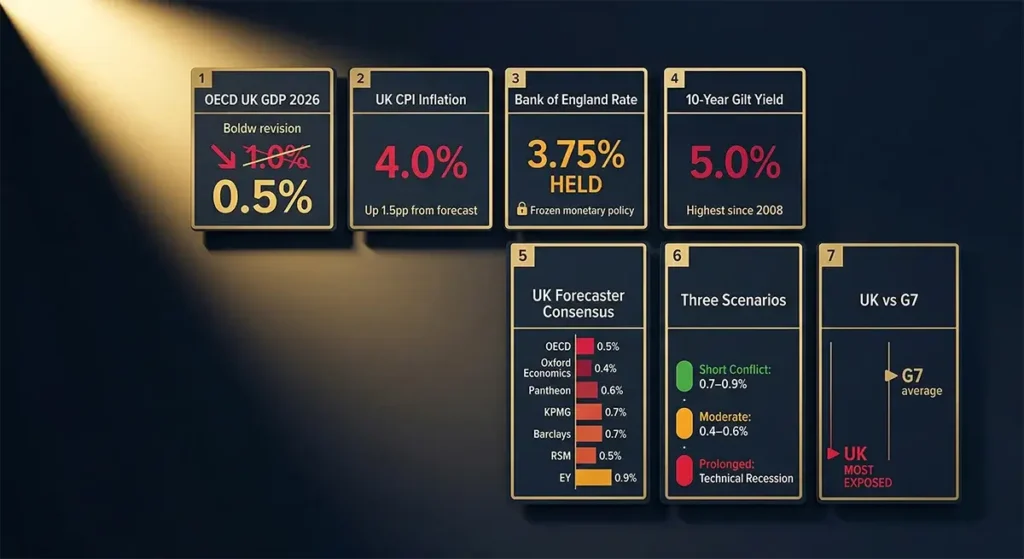

As of April 2026, the question of whether the UK is heading for a recession is no longer a theoretical worry confined to think tanks and academic economists. It is live, urgent, and actively being priced into gilt markets, mortgage rates, and business investment decisions across the country. The OECD has slashed its 2026 UK growth forecast to just 0.5% — the steepest revision of any major economy — and now projects UK inflation hitting 4%, up 1.5 percentage points from its December forecast. Forecasters at Barclays, KPMG, and Pantheon Macroeconomics have all cut UK growth projections to between 0.4% and 0.7%. The Bank of England held rates at 3.75% in March after markets had been expecting a cut — and traders are now pricing in the possibility of a rate hike before the year is out.

The UK is uniquely exposed to the 2026 global economic storm because three separate shocks are hitting simultaneously: the Iran war energy shock (for which the UK is more vulnerable than almost any other developed nation due to importing 44% of its energy), residual US tariff drag on exports and business confidence, and the pre-existing fiscal tightening from Chancellor Reeves’s Autumn 2025 Budget. RSM UK downside scenario puts growth at 0.5%. Oxford Economics forecasts just 0.4%. At that level, the margin between lethargic growth and a technical recession — two consecutive negative GDP quarters — is razor thin. The OECD has issued its starkest single-country warning for the UK of any G7 nation.

Why Britain Is More Exposed Than Almost Any Other Developed Economy

To understand why the OECD’s steepest single-country downgrade in its March 2026 interim economic outlook landed on the United Kingdom specifically, it is necessary to understand Britain’s particular structural vulnerabilities — vulnerabilities that pre-existed the Iran war and that the energy shock is now amplifying.

Energy import dependence at 44%: The UK imports approximately 44% of its total energy consumption — a structural weakness that the House of Commons Library identified as the primary reason Britain is “particularly exposed” to the Hormuz disruption. While the US, as the world’s largest oil producer pumping a record 13.6 million barrels per day, has meaningful domestic production to buffer against global price surges, the UK has no equivalent cushion. North Sea production, which once made the UK energy self-sufficient, has declined dramatically over the past two decades. The UK has negligible gas storage capacity compared to continental European competitors — a structural failure exposed brutally during the 2022 energy crisis and now exposed again. When Brent crude surges from $65 to $112 per barrel in five weeks, as it did between February 28 and early April 2026, UK consumers and businesses absorb the full shock at global market prices with no domestic production offset.

Gas market exposure through Dutch TTF: UK gas prices are linked to the European wholesale market through the Dutch TTF benchmark. The Iran war’s closure of the Strait of Hormuz also interrupted Qatar’s LNG exports — approximately 80% of Qatar’s LNG goes through Hormuz, and a significant portion was destined for European buyers. This has driven Dutch TTF gas benchmarks to nearly double to over €60 per megawatt-hour by mid-March 2026, with direct consequences for UK household energy bills, industrial production costs, and the government’s energy price cap mechanism. The Resolution Foundation has modelled that prolonged high gas prices could increase the energy price cap by £500 in July — a second consecutive annual energy cost shock hitting households already squeezed by the prior inflationary period.

Pre-existing fiscal constraint: Unlike the US, which has been running expansionary fiscal policy, or some European peers that retain more fiscal headroom, the UK government entered 2026 operating under strict self-imposed fiscal rules that Chancellor Rachel Reeves has described as “ironclad.” These rules — limiting government borrowing and targeting a declining path for the national debt — significantly constrain the government’s ability to respond to the energy shock with the kind of blanket household support measures deployed during the 2022 crisis (which cost approximately £40 billion). Reeves explicitly stated this week that there would be “no blanket measures to support households with their energy bills” in response to the Iran war. This fiscal restraint — prudent in normal times — means British households and businesses are absorbing more of the energy shock through direct price increases than they would in an alternative policy environment.

Starting from weakness, not strength: The UK entered the energy shock from a position of particular fragility. RSM UK’s analysis found the UK’s real economy — excluding public spending — ended 2025 in a technical recession: the sectors that produce goods and services had been contracting in H2 2025 even as nominal GDP stayed positive through public expenditure. The New Economics Foundation noted the shock was “coming on top of years of higher inflation” for UK households, who had not fully recovered purchasing power lost during the 2022-2023 inflationary period before the new supply shock arrived.

The Energy Shock’s Specific Impact on Britain: By the Numbers

The transmission of the oil and gas price surge into the UK economy operates through multiple simultaneous channels that compound one another.

Inflation trajectory revised sharply upward: Before the Iran war, UK CPI had been expected to fall from 3.0% in January 2026 toward the Bank of England’s 2% target from April 2026 onward, with a gentle decline toward 1.9% by mid-2027. That trajectory has been obliterated. The Bank of England’s Monetary Policy Committee stated on March 19 that CPI is now likely to be between 3% and 3.5% in Q2 and Q3 2026 due to higher energy prices — and that estimate already looks conservative if the Hormuz closure persists. The OECD projects UK inflation hitting 4% for 2026 — up 1.5 percentage points from its pre-war forecast and the largest single-country inflation revision in the OECD’s March interim report. Bloomberg’s estimates from ING and RSM UK suggest inflation could reach as high as 5% if current oil and gas prices are sustained — more than double the Bank of England’s 2% target.

Deutsche Bank’s Chief UK Economist Sanjay Raja warned in stark terms: “Inflation is poised for another unwelcome detour,” while ICAEW Chief Economist Suren Thiru described a “brutal inflation surge” as imminent. The February 2026 CPI reading of 3.0% — released on March 25 — was the last pre-war data point, and Zara Nokes of J.P. Morgan Asset Management captured the market’s view precisely: “UK inflation data is in effect old news, with attention now firmly on what is coming down the tracks as a result of the conflict in the Middle East.”

Growth forecasts cut across the board: The pace and breadth of UK growth forecast downgrades since the Iran war began is striking. The House of Commons Library research briefing catalogues the scale of the revisions with precision: the OBR had forecast 1.1% growth for 2026 before the conflict; Barclays and KPMG have since cut their forecasts to 0.7%; Pantheon Macroeconomics estimates a 0.8 percentage point hit over two years, leaving growth at just 0.6% in 2026; Oxford Economics forecasts only 0.4% growth; and the OECD itself now projects 0.5%. Every single forecaster has cut UK growth since February 28. Not one has revised upward.

| Forecaster | Pre-War UK GDP 2026 Forecast | Post-War Revised Forecast | Downgrade |

|---|---|---|---|

| OBR (Office for Budget Responsibility) | 1.1% | Under review | Significant |

| OECD | 1.0% | 0.5% | -0.5 pp |

| KPMG | 1.0% | 0.7% | -0.3 pp |

| Barclays | 1.1% | 0.7% | -0.4 pp |

| Pantheon Macroeconomics | 1.4% | 0.6% | -0.8 pp |

| Oxford Economics | N/A | 0.4% | Severe |

| EY ITEM Club | 0.9% | Under review | Risk of further cut |

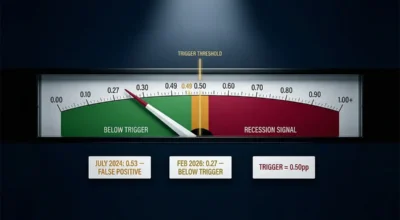

At 0.4–0.7% projected growth, the UK is operating in territory where any additional adverse shock — a worse-than-expected Hormuz closure, a second-round inflation spike, a consumer confidence collapse, or a disorderly gilt market — would be sufficient to tip consecutive GDP quarters into negative territory. The technical definition of recession is two consecutive quarters of negative GDP growth. At 0.5% annual growth distributed unevenly across quarters, the UK does not need a large additional shock to cross that line.

The Bank of England’s Impossible Dilemma

No institution in Britain faces a more challenging 2026 than the Bank of England — and the difficulty of its position is itself a risk factor for the UK economy. The Bank’s dual objectives of price stability (2% inflation target) and supporting the government’s economic policy (including growth) are in direct conflict as the energy shock simultaneously pushes inflation higher while weakening economic growth.

Before the Iran war, the MPC had been expected to cut rates at its March 19 meeting, continuing the gradual easing cycle that began in 2025. Instead, it held at 3.75%. In its statement, the MPC warned it was “alert to the increased risk of domestic inflationary pressures through second-round effects in wage and price-setting, the risk of which will be greater the longer higher energy prices persist.” The distinction between first-round effects (direct energy price rises in CPI) and second-round effects (businesses and workers building energy cost increases into broader price and wage decisions) is critical: first-round effects are temporary and the Bank typically looks through them; second-round effects are more persistent and the Bank is obligated to respond.

ING economist James Smith noted that Bank research suggests second-round effects become more pronounced when headline inflation exceeds 3.5–4% — a threshold that current projections suggest the UK is approaching. If second-round effects materialize — if businesses raise prices broadly to cover energy costs, and workers demand higher wages to cover higher living costs — the Bank faces a genuine rate-hiking imperative at the worst possible time for growth. Financial markets are already pricing in this possibility: the bond market has moved from pricing gradual rate cuts to pricing potential hikes by end-2026.

The gilt market signal is itself an additional warning. Since the start of the conflict, the 10-year UK gilt yield has risen from 4.2% to above 5% — hovering near its highest level since 2008. The 2-year gilt yield jumped from 3.5% to a peak of 4.6%. As AJ Bell investment director Russ Mould observed, the 10-year gilt is near 5% for only the third time since 2008 — with both previous occasions being moments of acute UK economic stress. For mortgage borrowers, the gilt market move is already materializing in product withdrawals and rate rises: banks and building societies have withdrawn over 1,500 mortgage products since February 28, and two-year fixed mortgage rates have risen from approximately 4.8% to 5.5%. For a borrower with a £200,000 mortgage over 25 years, this represents approximately £90 more per month — close to £1,000 per year — in additional costs.

The Bank of England’s inability to cut rates — or worse, its possible need to raise them — removes the key monetary policy support that would normally be deployed to cushion an economic slowdown. This “frozen in place” central bank is one of the most significant recession risk amplifiers for the UK economy specifically, compared to peers whose inflation profiles permit more policy flexibility.

The US Tariff Layer: A Pre-Existing Wound That Has Not Healed

The Iran war energy shock is arriving on top of a pre-existing trade headwind that the UK has been managing since 2025: the impact of US tariff policy on British exporters and business investment confidence.

While the UK secured a preferential trade arrangement with the United States — giving Britain somewhat less direct tariff exposure than the EU — the broader effects of US trade protectionism have been substantially negative for UK growth. KPMG’s UK Economic Outlook explicitly identifies “net trade” as “likely to remain weak” because “recent changes in US tariff policy will, on balance, make UK exporters less competitive in the face of higher trade barriers.” EY ITEM Club similarly cites tariffs and global uncertainty as “the leading drivers of subdued growth” alongside tight fiscal policy.

The deeper damage from US tariffs is not only direct — UK goods facing higher US import costs — but indirect, operating through three channels that KPMG and NIESR have both documented. First, global trade uncertainty reduces UK business investment: when companies cannot predict the trading environment, they defer capital allocation. The UK economy’s already-weak business investment was a primary reason growth stalled to 0.1% in consecutive quarters in late 2025, and tariff-induced uncertainty remains an ongoing suppressor. Second, a weaker global growth environment reduces demand for UK exports broadly, not only to the US. Third, the US-China trade war’s realignment of global supply chains creates competitive pressure on UK manufacturers as Chinese producers diverted from US markets seek alternative destinations.

The NIESR’s Winter 2026 economic outlook found that “delayed tariff effects and elevated uncertainty dampening investment” were contributing to a projected global growth slowdown to 3.2% in 2026 — with the UK’s open, trade-dependent economy more sensitive to global growth deceleration than larger, more internally-driven economies.

The Fiscal Squeeze: Rachel Reeves’s Unenviable Position

Chancellor Rachel Reeves faces a uniquely difficult fiscal environment. The 2025 Autumn Budget deployed National Insurance increases on employers that have contributed to a slowdown in UK hiring — the UK Factory PMI showed its worst supply chain stress since 2022 as of April 1, and the unemployment rate has been edging upward. The Budget’s planned fiscal consolidation — designed to restore credibility with gilt markets after the Liz Truss era’s 2022 shock — requires holding the line on spending and borrowing at precisely the moment when economic weakness and energy shock support needs are pushing in the opposite direction.

The gilt market is watching. The CNBC/OECD analysis noted that “with financial markets eyeing the UK’s Labour government closely for signs of fiscal indiscipline, Reeves reiterated that her ‘fiscal rules’ limiting government borrowing and lowering national debt were ‘ironclad.'” This fiscal credibility maintenance is not mere stubbornness — it reflects genuine awareness that another Liz Truss-style bond market rebellion would be catastrophically worse for UK households and businesses than the short-term pain of withholding energy support.

The New Economics Foundation has called on the government to deploy targeted support: shielding frontline public services through a central contingency fund, retaining the windfall tax on oil and gas companies, and accelerating micro-renewables rollout. These measures would be more fiscally disciplined than blanket household support while providing meaningful economic insulation. Whether the government moves in this direction will substantially affect how much of the energy shock translates into household spending cuts and economic contraction.

The Industrial and Supply Chain Damage

The Iran war’s impact on the UK economy extends beyond household energy bills into manufacturing and industrial supply chains in ways that the aggregate GDP numbers have yet to fully capture.

UK chemical and steel manufacturers — already among the most energy-intensive industrial sectors and the most exposed to global feedstock costs — have imposed surcharges of up to 30% to offset surging electricity and feedstock costs, according to the Wikipedia economic impact analysis. The concern raised by economists is that some of this damage could be permanent: if UK industrial companies cannot compete against international rivals with lower energy costs during the crisis period, some production capacity may be transferred overseas and never return — a process that economists characterize as “permanent deindustrialization.”

UK fertiliser production faces a specific structural problem: natural gas, which is 70–90% of ammonia production costs, has surged in price. British agricultural production — already under margin pressure — faces higher input costs for the 2026 growing season, with potential flow-through to food prices in Q3 and Q4 2026 that will add to headline CPI in the months when energy price shock second-round effects are also building.

The Bank of England’s April 2 warning that “UK firms lift price expectations on energy shock” captures the leading indicator: when firms signal they intend to raise prices, the second-round effects the MPC has been monitoring are materializing in advance data before they appear in official CPI statistics. The April 1 Bloomberg headline “UK Factory PMI Shows Worst Supply Chain Stress Since 2022” confirms the manufacturing sector is under acute pressure.

Three Scenarios for the UK Economy in 2026

With the full range of evidence assembled, three distinct economic scenarios can be defined for the UK through the rest of 2026, distinguished primarily by the duration of the Hormuz closure and the extent of second-round inflationary effects.

Scenario 1 — Short conflict, Hormuz reopens by May (25% probability per RSM UK’s assessment): If diplomatic or military developments reopen the Strait of Hormuz within the next 4–6 weeks, oil prices would fall from current levels back toward $80–$85, gas prices would begin declining, and UK inflation would peak near 3.5% before declining through H2 2026. GDP growth of 0.7–0.9% for the full year remains achievable. The Bank of England would likely hold rates at 3.75% for the remainder of the year before resuming cuts in early 2027. No recession — but a painful year of stagflationary pressure with household real incomes falling again.

Scenario 2 — Moderate conflict, Hormuz partially reopens mid-year (50% probability): The conflict persists through May–June with partial Hormuz reopening allowing some resumption of energy flows. Oil averages $110–$120 for Q2 before declining toward $85–$90 in H2. UK inflation peaks at 4.0–4.5%, the Bank of England holds or raises rates once by year-end, and GDP growth comes in at 0.4–0.6% for the full year. Individual quarters may briefly touch near-zero or marginally negative territory, producing significant public concern about recession without necessarily delivering the two consecutive negative quarters required for the technical definition. The OECD’s 0.5% growth forecast broadly reflects this scenario.

Scenario 3 — Prolonged closure through summer (25% probability, rising): The Strait of Hormuz remains effectively closed through June, July, and into the critical summer gas storage refill season for Europe. European gas storage — entering the crisis at just 30% capacity following a harsh 2025–2026 winter — fails to refill adequately. Oil reaches $130–$150. UK inflation breaches 5% as energy price cap rises by £500 in July. The Bank of England hikes rates to address second-round inflation anchoring risk, further compressing consumer spending and business investment simultaneously. GDP contracts in Q2 and Q3 2026. The UK enters a technical recession. The OECD characterizes this scenario as “high risk of technical recession if the maritime blockade persists through the summer refill season.”

The probability distribution across these three scenarios places the UK in a position where recession risk is genuine and quantifiable — not a tail risk to be dismissed — but also not yet the base case. The base case is continued anaemic growth that avoids the technical recession definition by the narrowest of margins, accompanied by real household income falls, mortgage cost increases, and a painful second inflation cycle.

The US Spillover Mechanism: Why American Recession Risk Matters for Britain

The UK’s recession risk cannot be assessed in isolation from the United States, the world’s largest economy and Britain’s largest single trading partner. If the US economy — where Goldman Sachs currently places 30% recession probability and Moody’s Analytics’ AI model sits at 49% — tips into contraction, the UK would face a global demand shock compounding its domestic energy and fiscal pressures.

The transmission channels from a US recession to the UK are well-documented and historically significant. Financial services — which account for approximately 10% of UK GDP and are deeply integrated with Wall Street through London’s role as a global financial hub — would face immediate revenue pressure from reduced deal flow, lower asset management fees, and higher credit losses. UK goods exports to the US would fall sharply in a US recession. The pound sterling would likely depreciate further against a safe-haven dollar, which would simultaneously worsen the UK’s already-elevated import inflation. Global risk sentiment deterioration would tighten UK financial conditions further, increasing corporate borrowing costs and suppressing investment.

Gita Gopinath, former IMF chief economist, calculated that every $10 sustained increase in oil prices above the pre-war baseline reduces global GDP growth by approximately 0.1–0.2 percentage points. At current prices — $50 above the pre-war baseline — that implies roughly 0.5–1.0 percentage points of global growth drag, which would be felt disproportionately in trade-dependent economies like the UK.

What This Means for UK Households and Businesses: Practical Guidance

For British households and businesses navigating the most uncertain UK economic environment since the 2022 energy crisis, the convergence of risks identified in this analysis has direct practical implications.

Mortgage borrowers — act on rate uncertainty now: With two-year fixed mortgage rates rising from 4.8% to 5.5% since the Iran war began, and with potential rate hikes rather than cuts now being priced by markets, households coming off fixed-rate deals in 2026 face a markedly different rate environment than they anticipated at the start of the year. Independent mortgage broker consultation to assess the rate-fixing strategy — whether to lock in current rates before potential further increases or to explore flexibility — is urgent for the roughly 1.5 million UK households with fixed deals expiring in 2026. For every £200,000 of outstanding mortgage, the difference between current rates and pre-war expectations represents up to £1,000 per year.

Energy costs — prepare for July price cap increase: The Resolution Foundation’s modelling suggests the energy price cap could increase by £500 in July if gas prices remain elevated. While the April reduction in green levies will provide temporary relief — pulling CPI down briefly before the underlying energy price shock reasserts itself — households should budget for higher energy costs from summer 2026. Smart meter installation, draught-proofing, and consumption reduction measures have better financial returns at £500+ annual cost increases than at lower cap levels.

Businesses — energy surcharges and supply chain review: UK businesses with energy-intensive operations should conduct urgent assessments of their energy cost exposure and hedging position. Those with long-term energy contracts locked in before the crisis are relatively protected; those on variable or spot pricing face margin compression that KPMG’s analysis suggests is already prompting surcharging across chemical and steel sectors. Supply chains with significant Middle East exposure — fertilisers, petrochemicals, helium for semiconductor manufacturing — require review for alternative sourcing or buffer stock strategies.

Investors — gilt yields and defensive positioning: The 10-year gilt yield above 5% for the first time since 2008 creates both a risk and an opportunity signal. The elevated yield reflects genuine stagflation risk premia — the market is pricing the possibility that the Bank of England needs to raise rates into a weakening economy, an outcome that would be highly negative for UK growth assets. For investors with UK equity or property exposure, the capital economics case for hedging with defensive instruments or increasing cash holdings as a buffer against the Scenario 3 recession case is stronger now than at any point since the 2022 mini-budget crisis.

The OECD Verdict: Britain’s Unique Vulnerability in Context

The OECD’s March 2026 interim economic outlook stands as the most authoritative single international assessment of the UK’s position. Its conclusion — the steepest growth downgrade and the steepest inflation upgrade of any G7 economy — was not coincidental. It reflected the specific combination of structural vulnerabilities, pre-existing weakness, and policy constraints that make Britain more exposed to the triple shock of energy, tariffs, and US slowdown than its peers.

Among the G7, the ranking of vulnerability as implied by the OECD revisions places the UK and Germany at the most exposed end — the UK through energy dependence and pre-existing fragility, Germany through industrial energy intensity. The US, despite running higher recession probability estimates from Goldman and Moody’s, benefits from being the world’s largest oil producer and from a position of fiscal flexibility that the UK does not currently possess. Japan and Canada occupy intermediate positions. France and Italy face significant risks but were already discounting more adverse growth environments before the crisis.

The OECD’s core conclusion for the UK is captured in its March report: growth of 0.5% this year, inflation of 4%, and a warning that “energy-intensive economies face high risks of technical recession if the maritime blockade persists through the summer refill season.” For Britain in April 2026, that warning is the single most important economic sentence in circulation — because the summer refill season begins in six weeks, and the Strait of Hormuz remains closed.

💬 0 Comments