In a period of elevated recession risk like 2026, one of the most anxiety-provoking unknowns for households and businesses is simply: how long will a potential recession last? The gap between a brief two-quarter contraction and a prolonged multi-year depression is financially enormous — it is the difference between drawing down three months of emergency reserves and needing two years of financial cushioning. This comprehensive guide answers the question definitively using every documented US recession since 1854, explaining what drives recession duration, what the data shows about typical lengths, and what the specific characteristics of a 2026 recession might suggest about its potential duration.

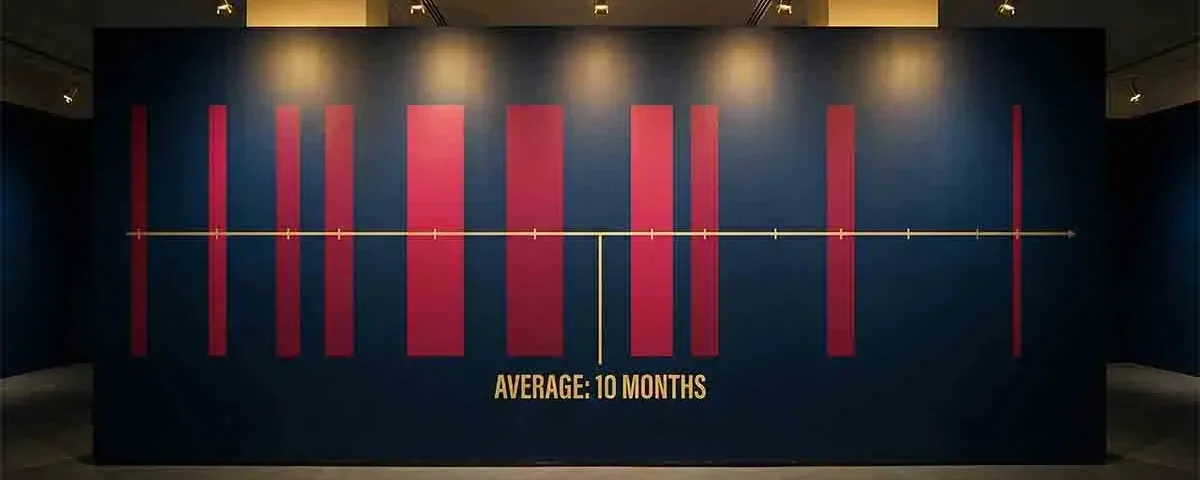

The average US recession since World War II has lasted approximately 10 months from peak to trough. The median is approximately 10 months as well, reflecting a relatively consistent range of 6–18 months for most post-war recessions. Only three post-war recessions exceeded 18 months: the 1973–1975 oil embargo recession (16 months), the 2007–2009 financial crisis (18 months), and by some measures, the 1981–1982 recession (16 months). Modern monetary and fiscal policy tools have generally limited recession duration relative to the pre-war era — making the post-1945 data more relevant for 2026 planning purposes than the full 170-year historical record.

The Complete US Recession History: Every Documented Contraction Since 1854

The NBER’s Business Cycle Dating Committee has documented US business cycle peaks and troughs since 1854 — providing 34 recession episodes whose duration can be analyzed. Understanding the full dataset, and especially the subset of post-World War II recessions, provides the most reliable foundation for recession duration planning.

Post-World War II Recessions: The Relevant Modern Dataset

| Recession Period | Start (Peak) | End (Trough) | Duration (Months) | Primary Cause |

|---|---|---|---|---|

| 1945 Reconversion | Feb 1945 | Oct 1945 | 8 | Post-WWII demobilization and production cutback |

| 1948–1949 | Nov 1948 | Oct 1949 | 11 | Post-war inventory adjustment; credit tightening |

| 1953–1954 | Jul 1953 | May 1954 | 10 | Post-Korean War defense spending reduction |

| 1957–1958 | Aug 1957 | Apr 1958 | 8 | Fed tightening; investment decline |

| 1960–1961 | Apr 1960 | Feb 1961 | 10 | Credit tightening; inventory cycle |

| 1969–1970 | Dec 1969 | Nov 1970 | 11 | Fed tightening to combat inflation; Vietnam spending winds down |

| 1973–1975 | Nov 1973 | Mar 1975 | 16 | Oil embargo; stagflation; Nixon shock |

| 1980 | Jan 1980 | Jul 1980 | 6 | Volcker rate shock; credit controls; oil price spike |

| 1981–1982 | Jul 1981 | Nov 1982 | 16 | Volcker Fed rate tightening to break inflation |

| 1990–1991 | Jul 1990 | Mar 1991 | 8 | S&L crisis; oil price spike; Gulf War uncertainty |

| 2001 | Mar 2001 | Nov 2001 | 8 | Dot-com bust; 9/11 shock; capital expenditure collapse |

| 2007–2009 | Dec 2007 | Jun 2009 | 18 | Housing bubble collapse; financial system crisis; credit crunch |

| 2020 | Feb 2020 | Apr 2020 | 2 | COVID-19 pandemic shutdown; unprecedented fiscal/monetary response |

Statistical Summary: Post-War Recession Duration

| Statistical Measure | Duration (Months) |

|---|---|

| Average (mean) — all post-war recessions | 10.1 months |

| Median — all post-war recessions | 10.0 months |

| Shortest recession (2020 COVID) | 2 months |

| Longest recession (2007–2009) | 18 months |

| Most common range | 8–11 months |

| Recessions under 12 months | 10 of 13 (77%) |

| Recessions 12 months or longer | 3 of 13 (23%) |

Pre-War vs Post-War: Why Modern Recessions Are Shorter

The full historical record from 1854 through 1945 shows significantly longer average recession duration — approximately 21 months for the pre-war period versus 10 months post-war. This dramatic improvement reflects four structural changes in the post-war economy that did not exist in the 19th and early 20th centuries:

Active monetary policy: The Federal Reserve, established in 1913 but significantly empowered by the Banking Acts of 1933 and 1935, can now cut interest rates rapidly and deploy a range of liquidity and asset purchase tools to arrest financial panics and stimulate credit availability. The 19th-century economy had no central bank with this capability — financial panics cascaded unimpeded into prolonged depressions. The Fed’s 2008–2009 response (cutting rates to zero, deploying quantitative easing, creating emergency lending facilities for commercial paper, money market funds, and primary dealers) almost certainly shortened that recession significantly from what a laissez-faire response would have produced.

Automatic fiscal stabilizers: Unemployment insurance (established 1935), Social Security (established 1935), and the broader federal safety net automatically inject spending into the economy when employment falls — without requiring any new legislative action. These automatic stabilizers reduce the depth and duration of demand contractions by maintaining income flows to households whose employment income has been interrupted. In the 19th century, no such stabilizers existed — unemployed workers had zero government income support, causing immediate consumption collapse that deepened every recession.

FDIC deposit insurance: Bank runs — a primary amplifier of pre-FDIC recessions — have been effectively eliminated by federal deposit insurance. The 1930–1933 banking panic, during which over 9,000 banks failed and millions of Americans lost their deposits, amplified the Great Depression from a severe recession into a catastrophic multi-year depression. Post-FDIC, bank failures are orderly, insured depositors are protected, and the cascading bank run dynamic has not recurred at systemic scale.

Global trade and financial integration: The post-war international monetary system (Bretton Woods, its successors, and the WTO framework) has reduced the beggar-thy-neighbor protectionist dynamics that amplified the Great Depression — though the 2025–2026 tariff regime represents some reversal of this integration, introducing supply-side inflationary risk that was characteristic of the 1970s stagflation period.

What Drives Recession Length: The Key Variables

Examining the post-war recession history reveals consistent patterns in the factors that determine whether a recession is brief (6–10 months) or prolonged (12–18+ months):

Financial system health: The single most powerful determinant of recession length is whether the financial system (banks, shadow banks, credit markets) is functioning or impaired. The two longest post-war recessions — 1973–1975 and 2007–2009 — both involved significant financial system stress: the 1973–1975 recession involved the Franklin National Bank failure and significant banking stress alongside the oil shock; 2007–2009 was explicitly a financial system crisis. The 2001 recession, by contrast, was primarily a capital expenditure collapse with a relatively healthy banking system — it lasted only 8 months despite a severe stock market decline. The 1980 recession was also brief (6 months) because the credit controls implemented were deliberately temporary and removed quickly. When credit channels remain open, recessions tend to be shorter because economic actors can borrow through the downturn and recover faster when conditions improve.

Policy response speed and scale: The COVID-19 recession (2 months — the shortest in recorded US history) demonstrates how an overwhelming, rapid policy response can produce an exceptionally brief downturn. The combination of $2.2 trillion in the CARES Act, Federal Reserve balance sheet expansion from $4 trillion to $9 trillion in 12 months, $600 enhanced weekly unemployment benefits, PPP loans to businesses, and direct stimulus payments to households injected an unprecedented volume of economic support in an unprecedented timeframe. The 2020 recession’s brevity is not replicable in every scenario — it was specifically enabled by the ability to deploy massive fiscal and monetary support in an environment where the downturn’s cause (pandemic) was clearly temporary and reversible. An inflation-constrained recession (like the 2026 stagflation scenario) limits the Fed’s ability to replicate this response.

The nature of the triggering shock: Supply-side shocks (oil embargo, pandemic shutdown) tend to produce sharp but briefer recessions if the shock itself is temporary. Demand-side financial crises (debt bubbles, banking crises) tend to produce longer recessions because the debt overhang deleveraging process takes years rather than months. The 2026 potential recession appears driven by a combination of tariff-driven supply-side inflation and demand-side credit deterioration — a mixed trigger whose duration implications are uncertain but potentially closer to the 12–18 month range than the 6–8 month brief recession range.

Labor market rigidity: Economies where labor markets adjust slowly (due to structural factors, geographic immobility, skills mismatches, or regulatory constraints) tend to experience longer recessions — the unemployment created during the contraction takes longer to reverse, and the human capital costs of prolonged unemployment create lasting economic damage that slows recovery.

Recession Length vs Recovery Length: An Important Distinction

Understanding recession duration requires distinguishing between the recession itself (peak to trough — the contraction period) and the recovery (trough to return to prior peak — the expansion back to pre-recession economic levels). These are different time periods with dramatically different lengths.

While the average post-war recession lasted approximately 10 months, the average recovery to prior economic peak took significantly longer — often 12–24 months for mild recessions and 36–60+ months for severe ones. The 2007–2009 recession itself lasted 18 months, but employment did not return to pre-recession levels until approximately 2014 — a 77-month total labor market recovery, far longer than the recession itself. Personal income, housing values, and household net worth recovery times were similarly extended.

For financial planning purposes, the relevant question is not just “how long is the recession?” but “how long before my specific financial situation returns to pre-recession baseline?” This is typically longer than the recession itself — particularly for workers who experienced unemployment during the downturn (average weeks unemployed during recessions: 16–24 weeks for mild recessions, 25–40+ weeks during severe ones).

What History Suggests About a Potential 2026 Recession’s Duration

Applying the duration determinants to the current 2026 economic environment, several factors suggest a potential 2026 recession would most likely fall in the 10–16 month range rather than the brief 6–8 month or prolonged 18+ month extremes:

Factors suggesting a moderate duration (10–14 months): The financial system is not in crisis — banks are adequately capitalized, there is no subprime-style hidden leverage in the system, and credit markets continue to function despite tightening conditions. Consumer and corporate balance sheets entered 2026 with stronger equity positions than 2007. The Federal Reserve retains the ability to cut rates (though constrained by inflation) and has the full QE toolkit available if conditions deteriorate significantly.

Factors suggesting potentially longer duration (14–18 months): The tariff-driven inflation constrains the Fed’s ability to respond aggressively — the central bank cannot cut rates as rapidly or as deeply as it could in 2001 or 2008 without risking reigniting inflation that itself reduces consumer spending. Credit card delinquency rates at historical highs suggest a consumer sector already under significant financial stress entering any recession — less buffer capacity than in prior cycles. The housing market’s transaction freeze (not a price crash, but a volume collapse) will be slow to resolve, limiting housing-related economic activity recovery. Global trade disruption from tariffs reduces the export support that helped some prior US recoveries.

Factors suggesting potentially shorter duration (6–10 months): Congress could reverse the tariff regime that is a primary 2026-specific stress driver — unlike most recession causes, this one is addressable through policy reversal more rapidly than debt deleveraging or bank recapitalization. Strong labor market fundamentals (low structural unemployment, high prime-age participation) provide a foundation for rapid employment recovery once demand conditions improve.

How to Plan Your Emergency Fund for Recession Duration

The recession duration data has direct practical implications for emergency fund sizing. A 10-month average recession suggests a baseline of 6 months of essential expenses in liquid reserves for most employed households — providing buffer for a potential layoff during the recession plus the job search period that typically extends beyond the formal recession’s trough. For households in recession-vulnerable industries (hospitality, construction, advertising, retail, media) or in single-income situations, 9–12 months of reserves is the more appropriate target given the historical range of recession durations and the reality that unemployment typically peaks after the official recession end date.

The NBER recession trough is the moment economic conditions stop deteriorating — not the moment the economy returns to pre-recession health. Unemployment typically continues rising for 3–6 months after the official recession ends, meaning the financial stress on households extends well beyond the technical recession period. Planning for this post-trough vulnerability period is as important as planning for the recession itself.

💬 0 Comments