On the morning of April 14, 2026 — as finance ministers, central bank governors, and the heads of the world’s largest corporations gathered in Washington DC for the IMF and World Bank spring meetings — one voice cut through the diplomatic hedging and institutional scenario-modeling with striking directness. Ken Griffin, the founder and CEO of Citadel, one of the most profitable hedge funds in history, took the stage at the Semafor World Economy Summit and delivered a warning that immediately reverberated across financial markets globally.

“Let’s assume the Strait is shut down for the next six to 12 months,” Griffin said on stage, speaking about the Strait of Hormuz, which has been effectively closed since March 4, 2026 following US and Israeli military strikes on Iran. “The world’s going to end up in a recession. There’s no way to avoid that.”

For context: Ken Griffin is not a commentator. He is not a politician managing messaging. He is the founder of Citadel LLC — a firm that manages approximately $67 billion in assets under management, has generated $83 billion in net gains for investors since its founding in 1990, and whose flagship Wellington strategy has delivered annualized returns placing it among the most consistently profitable multi-strategy funds in the history of the hedge fund industry. Griffin has a net worth of approximately $51.2 billion as of January 2026, making him the 34th-wealthiest person on earth. He also founded Citadel Securities, which handles roughly one-quarter of all US stock trades — meaning his firm sits at the literal center of American financial market infrastructure and has real-time visibility into capital flows, risk pricing, and economic stress that no government institution can match.

When a person of this specific institutional standing, with this specific information advantage, uses the phrase “there’s no way to avoid” a global recession if a specific condition persists for six to twelve months — that statement demands serious analysis. This cornerstone guide provides it: who Ken Griffin is and why his warning carries more weight than most, the full context of what he said and where he said it, the six-to-twelve-month timeline and what it means economically, what other major voices said at the same forum, the data that supports or complicates his assessment, and what his warning means practically for American investors and households.

Citadel CEO Ken Griffin issued an explicit global recession warning on April 14, 2026 at the Semafor World Economy Summit in Washington DC, stating that a Strait of Hormuz closure lasting six to twelve months would produce a global recession with “no way to avoid” it. Griffin manages $67 billion at Citadel and is worth $51.2 billion — his firm processes roughly 25% of all US stock trades, giving him market intelligence that is genuinely unmatched. His warning was corroborated on the same day by the IMF’s World Economic Outlook severe scenario (below 2% global growth), Rapidan Energy’s Bob McNally (“guaranteed global recession”), and Lazard CEO Peter Orszag’s “Road Runner moment” framing. The key variable is time: the longer the Strait remains restricted, the more certain Griffin’s forecast becomes.

Who Is Ken Griffin? Why His Warning Commands Attention

Understanding why Griffin’s Hormuz recession warning is qualitatively different from the dozens of recession warnings circulating in April 2026 requires understanding who he actually is — beyond the headline net worth figure that typically appears in financial media.

Kenneth Cordele Griffin was born on October 15, 1968, in Daytona Beach, Florida, and raised in a middle-class household. He began trading convertible bond arbitrage from his Harvard University dormitory room in 1987 — securing a satellite dish for real-time stock quotes and funding his initial trades with $265,000 from his grandmother and a high school friend. When the market crashed in 1987, Griffin was buying, not selling, and made money. He graduated Harvard in 1989 with a degree in economics and launched Citadel officially on November 1, 1990, with $4.6 million in initial assets.

What followed is the defining story of self-made financial institution-building in modern American history. Citadel grew from $4.6 million to approximately $67 billion in assets under management as of early 2026 — after returning nearly $5 billion in 2025 profits to investors before the year-end. The firm’s flagship Wellington strategy has delivered returns that place it among the all-time top-performing multi-strategy funds globally. Citadel’s most profitable single year was 2022 — the year of the Russia-Ukraine war and the post-COVID inflation surge — when it generated $16 billion in net gains for investors, the largest single-year dollar return in hedge fund history to that point. Total net gains for investors since inception have reached $83 billion. The firm relocated its headquarters from Chicago to Miami in 2022.

Citadel Securities — Griffin’s market-making arm, distinct from the hedge fund — is arguably an even more remarkable institution. It handles approximately one-quarter of all US stock trades, making it the largest retail equity market maker in the United States. Citadel Securities generated a record $9.7 billion in trading revenue in 2024. It was valued at $22 billion in a 2022 funding round with Sequoia Capital and Paradigm. Griffin owns approximately 80% of Citadel Securities — a stake that alone accounts for roughly $17 billion of his net worth.

The relevance of all this institutional context to Griffin’s Hormuz warning is direct: Citadel Securities processes the order flow of tens of millions of retail investors and institutional funds every single trading day. It sees, in real time and in aggregate, how capital is moving, how risk is being priced, which sectors are receiving inflows and which are facing redemptions, and where the stress fractures in market infrastructure are appearing. Griffin’s view of global economic risk is not formed from reading news reports or modeling spreadsheets — it is formed from observing the actual behavior of capital at institutional scale, every market hour, continuously.

When Griffin says six to twelve months of Hormuz closure means a recession is inevitable, he is expressing a judgment informed by the most comprehensive real-time economic intelligence available to any private actor on earth. That is why his warning belongs in a different analytical category from institutional forecasts, survey-based projections, or media commentary.

The Setting: Semafor World Economy Summit, April 14, 2026

Griffin’s warning was delivered in a setting that amplified its significance beyond the specific content of his remarks. The Semafor World Economy Summit, held annually in Washington DC, is described by Semafor as “the largest gathering of top global CEOs in North America.” The April 2026 edition drew more than 500 participants — global CEOs, finance ministers, US cabinet secretaries (including Treasury Secretary Scott Bessent and Commerce Secretary Howard Lutnick), central bank governors, and senior executives from Goldman Sachs, Citadel, Hyundai, Eli Lilly, Anthropic, TotalEnergy, and dozens of other major institutions.

The summit’s timing — scheduled to coincide with the IMF and World Bank spring meetings in Washington — placed Griffin’s remarks in direct conversation with the IMF’s own April 14 World Economic Outlook release, which on the same day issued its own severe scenario warning of below-2% global growth. The co-occurrence of Griffin’s “no way to avoid” recession warning and the IMF’s “close call for global recession” severe scenario, on the same day, in the same city, before overlapping audiences of global economic decision-makers, created an unusually powerful convergence of institutional and private-sector analysis pointing in the same direction.

Also speaking at the Semafor summit was Chicago Fed President Austan Goolsbee, who participated in a panel discussion on monetary policy. The Federal Reserve Bank of Chicago confirmed Goolsbee’s participation in a panel also featuring Central Bank of Ireland Governor Gabriel Makhlouf — a gathering that represents the degree to which the Semafor event has become a genuine convening of global economic policy authority, not merely a high-end networking event.

Griffin’s Exact Words: The Full Quote Context

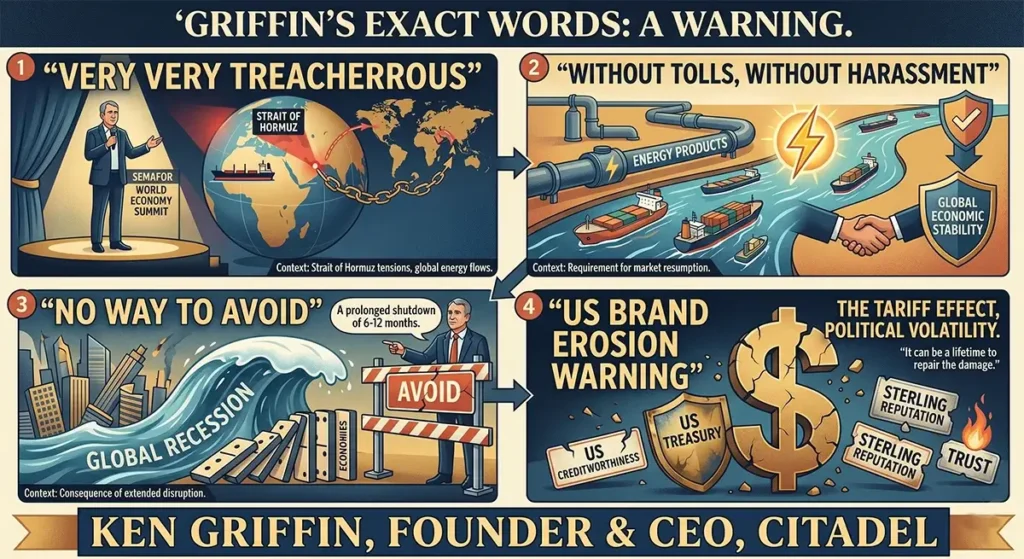

Griffin made three distinct and quotable statements at the Semafor summit that together constitute his complete assessment. They deserve to be read in sequence, as each adds essential context to the others.

First, his characterization of the current moment: “This really is a very, very treacherous moment for the world economy.” The specific repetition of “very, very” is notable — Griffin is not given to rhetorical excess, and the doubling of the intensifier suggests he is deliberately emphasizing the severity of his assessment against what he perceives as market and public complacency.

Second, his definition of the essential economic variable: “From a macroeconomic perspective around the world…the key criteria is the resumption of the continued flow of energy products from the Middle East without tolls, without harassment.” This statement is economically precise in a way that distinguishes Griffin’s analysis from most public commentary. He is not saying the key criterion is a ceasefire, or political negotiations, or geopolitical stability in the abstract. He is saying the key criterion is specifically the physical flow of energy products — and he adds two specific qualifiers that complicate the ceasefire picture: without tolls and without harassment. Iran’s Revolutionary Guard had been demanding that vessels pay cryptocurrency-denominated tolls to transit the Strait, and even under the fragile April 8 ceasefire, harassment of non-Iranian tankers remained a reported condition. Griffin’s framing thus implies that even a nominal ceasefire that does not restore fully free, unencumbered transit of the Strait fails his essential criterion.

Third, and most definitively, his recession verdict: “Let’s assume [the Strait is] shut down for the next six to 12 months — the world’s going to end up in a recession. There’s no way to avoid that.” This is as explicit as economic forecasting ever gets from a major market participant. “No way to avoid” is not a probability estimate with error bars. It is a categorical statement of certainty, conditional on a specific time frame. Griffin is saying that if the closure persists for six to twelve months, recession is not a risk to be managed — it is a destination that is already determined by the physics of the global energy system.

He also commented on the United States’ broader geopolitical standing, noting that the US “was an aspiration for most of the world” and that “we’re eroding that brand right now” — adding that the president, Treasury secretary, and Commerce secretary “need to be very thoughtful…because when you tarnish that brand, it can be a lifetime to repair the damage that has been done.” This broader observation contextualizes Griffin’s recession warning within his view that the geopolitical choices that led to the Hormuz closure carry costs beyond the energy shock itself — costs measured in the long-term credibility and influence of the United States in global economic affairs.

The Six-to-Twelve Month Timeline: What the Math Actually Says

Griffin’s six-to-twelve-month threshold deserves quantitative scrutiny. Why is that specific timeframe the recession trigger? The answer lies in the interaction between strategic petroleum reserve capacity, supply chain adaptation timelines, and the cumulative damage that sustained high energy costs inflict on household purchasing power, business investment, and central bank policy flexibility.

The IEA’s unprecedented release of 400 million barrels from strategic reserves — announced on March 11, 2026, the largest in IEA history — represents the primary buffer between the current partial disruption and the full economic consequences of sustained Hormuz closure. The IEA reports that its member countries collectively hold approximately 1.2 billion barrels of public emergency oil stocks plus approximately 600 million barrels of industry stocks held under government obligation — a total buffer of roughly 1.8 billion barrels. At current global consumption of approximately 100 million barrels per day, and with a disruption removing approximately 15 million barrels per day of Gulf exports (the gap between 20 million barrels flowing through Hormuz and the 5 million barrels per day of maximum alternative bypass capacity), the strategic reserve buffer covers approximately 120 days — four months — before it begins running critically low.

By Griffin’s six-month threshold, the strategic reserve buffer has been significantly drawn down, the “ships-already-in-transit” inventory effect has fully worked through the system, and economies are facing the raw energy cost of the disruption without any buffer absorption. By the twelve-month mark, the supply chain adjustments that take time to implement — new pipeline capacity, renewable energy acceleration, alternative LNG supply development — are still largely incomplete (most new infrastructure takes 2–5 years to bring online), while the full second-round inflationary effects of sustained energy prices above $100/barrel have worked through wages, services pricing, and business investment decisions.

Oxford Economics modeled a related threshold independently, finding that global oil prices averaging $140 per barrel for two months would be “economically overwhelming” — a “breaking point” that would push the eurozone, the UK, and Japan into contraction and create an economic standstill in the US. At $100/barrel sustained for six months, the damage accumulates more gradually but ultimately exceeds the $140/barrel two-month shock in total economic harm. Both paths lead to Griffin’s destination; the only difference is the route.

Corroborating Voices: A Wall of Expert Consensus

Griffin’s warning is striking precisely because it aligns with — and in some formulations exceeds — assessments from multiple institutional and expert voices who reached the same conclusion through different analytical frameworks on approximately the same timeline.

Bob McNally, Rapidan Energy Group: McNally — the founder of the Rapidan Energy consulting group and a former energy policy advisor to President George W. Bush — stated directly to CNBC on March 2, 2026: “A prolonged closure of the Strait of Hormuz is a guaranteed global recession.” The word “guaranteed” is even stronger than Griffin’s “no way to avoid” — and McNally made this statement ten days earlier, when the closure was only days old. His framing as a “guarantee” rather than a probability reflects the same physical-supply logic that underpins Griffin’s analysis: the math of 20 million barrels per day removed from a 100-million-barrel-per-day global supply is not a probabilistic estimate, it is an arithmetic certainty that plays out in real economic pain over time.

Peter Orszag, CEO of Lazard: Also speaking at the Semafor World Economy Summit the day before Griffin (April 13), Orszag offered a complementary frame. He described the current moment as a “Road Runner moment” — invoking the cartoon physics where Wile E. Coyote runs off a cliff without immediately falling. “Because of the combination of the ships that were already through the Strait of Hormuz before the war began, and existing inventories making up for the drop in shipments, the impact of what’s happening is not yet manifest itself in most economies,” Orszag said. “Supply shocks take a very long time to feed through into prices. That was true for COVID. It’s true with regard to tariffs. It will be true with regard to the Middle East.” Orszag’s Road Runner analysis is actually more alarming than it might appear: he is saying the economic damage is already locked in by physics and will arrive regardless of what happens diplomatically — the only question is when the cartoon character looks down and realizes gravity has been operating the entire time.

Orszag also articulated the US geopolitical dilemma with precision, noting that Washington finds itself “in a little bit of a box” with three paths forward: a military ground operation to reopen the Strait (which may not achieve the desired outcome); a negotiated settlement involving China as an intermediary (which would make Beijing a “backdoor power broker” with enhanced global standing); or declaring victory without the Strait being fully reopened (which would effectively empower Iran). None of these paths is clean. All of them carry either economic or geopolitical costs that extend well beyond the immediate energy shock.

The IMF’s April 2026 WEO Severe Scenario: Released on the same day as Griffin’s remarks, the IMF’s severe scenario — oil at $110/barrel in 2026 rising to $125/barrel in 2027 — predicts global growth falling below 2%, which the IMF characterizes as “a close call for a global recession which has happened only four times since 1980.” Global inflation would top 6% in this scenario. “A number of countries would be in outright recessions,” IMF Chief Economist Pierre-Olivier Gourinchas stated. The IMF’s severe scenario and Griffin’s six-to-twelve-month recession prediction are not identical — Griffin’s threshold implies a particular duration condition — but they describe the same destination through different analytical routes.

Goldman Sachs: Goldman’s economists raised their twelve-month US recession probability by 5 percentage points to 25% early in the crisis, after oil flows were disrupted for a full month and crude averaged $110 in March and April. In a more extreme scenario, Goldman modeled inflation at 3.3% and GDP at 2.1% — and these were early-crisis estimates before the sustained closure dynamics that Griffin’s six-to-twelve-month framing addresses.

Macquarie Group: The investment banking firm estimated that if the ceasefire fails to hold and hostilities continue into June, oil has a 40% chance of reaching $200 per barrel — a level that would exceed even the IMF’s severe scenario assumptions and that would make Griffin’s recession prediction not merely probable but arithmetically certain in a much shorter timeframe than six months.

What “Without Tolls, Without Harassment” Actually Means

Griffin’s specific language about the essential criterion — resumption of energy flows “without tolls, without harassment” — deserves particular analytical attention because it reveals his assessment of why the April 8 ceasefire is insufficient to resolve the economic risk he is describing.

Iran’s Revolutionary Guard had reportedly demanded that vessels transiting the Strait pay tolls denominated in cryptocurrency — a demand that, if enforced, would represent a fundamental restructuring of international maritime law and a direct economic benefit to Iran from the very trade it was theoretically restricting. Even under the fragile ceasefire announced April 8, the status of these toll demands remained unresolved, and reports of harassment of non-Iranian tankers continued. War-risk ship insurance premiums for Hormuz transit had risen from 0.125% of vessel value per transit before the conflict to 0.2–0.4% — a premium that remains elevated under ceasefire conditions because insurers price the ongoing threat, not merely the immediate incident rate.

Griffin’s “without tolls, without harassment” criterion implies that partial reopening — ships technically transiting but under Iranian supervision, with toll payments, or at reduced frequency due to ongoing risk pricing — does not satisfy the economic recovery condition. The global oil market requires predictable, insurable, unencumbered flow of approximately 20 million barrels per day through the Strait to function at its pre-crisis equilibrium. Anything less perpetuates supply constraints, elevated prices, and the economic damage those prices inflict on consuming economies. In this framing, a ceasefire that does not restore full freedom of navigation is economically indistinguishable from no ceasefire at all — merely a slower version of the same destination Griffin is warning about.

Citadel’s Own Positioning: What Griffin’s Fund Is Doing

Beyond the macro warning, the question of what Citadel itself is doing in the current environment provides a complementary lens on Griffin’s conviction. Prior to the Iran war, Citadel had made significant high-profile long positions in major technology companies: the fund added approximately $2.52 billion in Amazon stock in early 2026, taking its Amazon position to over $3.2 billion, while also expanding its Nvidia stake to nearly $4 billion — reflecting Griffin’s conviction in the AI investment cycle as a structural growth driver independent of the geopolitical situation.

This technology conviction is relevant to interpreting his Hormuz warning: Griffin is not a perma-bear or a reflexive doom-predictor. He entered 2026 with large, confident bets on AI-driven economic growth. His recession warning is therefore a conditional overlay on an otherwise constructive economic view — he believes in the structural technology tailwinds, AND he believes that a sustained Hormuz closure would override those tailwinds with an energy shock severe enough to produce recession regardless of underlying economic momentum. This conditional structure — “everything else being positive, the energy shock is still strong enough to cause recession if it lasts long enough” — is the most analytically significant aspect of his April 14 statement.

Historical Precedent: When Major Investors Called It Right

Part of what makes Griffin’s warning credible is its structural similarity to calls that proved correct in prior energy shock episodes. The 1973 Arab oil embargo produced a disruption of approximately 7–10% of global oil supply; the 2026 Hormuz closure has effectively disrupted approximately 20% — more than double the scale. Major economic analysts who warned about the 1973 shock’s recessionary implications were broadly correct: the US entered recession in November 1973, oil-importing economies across Europe and Asia followed, and the damage persisted through 1975.

The 1979 Iranian Revolution oil shock produced a second episode. Analysts who correctly modeled the 1979 shock’s persistence — arguing that the supply disruption would be sustained long enough to produce durable inflationary and recessionary consequences — were validated by the 1980 recession and the necessity of Paul Volcker’s historically aggressive monetary response. In both cases, the key analytical insight that distinguished correct recession predictions from incorrect “temporary blip” assessments was precisely the duration assumption: those who correctly estimated the shock would be sustained for six months or more were broadly correct about the recession outcome; those who assumed rapid resolution were wrong.

Griffin’s six-to-twelve-month threshold is essentially applying this historical calibration to the 2026 episode. He is saying: if the Hormuz closure resembles the brief 1973 episode (which ultimately resolved after about five months of embargo), the damage is severe but potentially recoverable. If it resembles the extended 1979 disruption or exceeds it in duration, recession becomes unavoidable by the mechanics of cumulative energy cost damage, second-round inflation, central bank policy constraints, and the exhaustion of strategic reserve buffers.

The US Brand Argument: Griffin’s Second Warning

Griffin’s geopolitical observation — that the US is “eroding that brand right now” — is not a tangential remark. It is connected to his economic analysis in a way that becomes clearer when read alongside Orszag’s “box” framing of US diplomatic options.

The United States’ ability to convene the global economic response to the Hormuz crisis — to coordinate IEA reserve releases, to maintain the dollar’s reserve currency status, to lead the diplomatic negotiations that determine whether the crisis resolves in weeks or months — depends critically on what Griffin calls “the brand”: the perception among global governments, markets, and institutions that the US is a reliable, rational, and consistently principled actor in global economic and geopolitical affairs. When that perception erodes — through unpredictable policy shifts, adversarial treatment of allies, or actions that suggest US decision-making is driven by domestic political considerations rather than considered strategic judgment — the US loses the institutional authority that makes its leadership of global crisis response credible and effective.

Griffin is warning, in other words, that the economic cost of the Hormuz closure is not purely a function of the physical supply disruption. It is also a function of the US’s ability to organize a coordinated global response — and that ability is itself a function of the geopolitical credibility that he believes is currently being damaged. The erosion of “the brand” does not simply produce diplomatic awkwardness; it translates into harder economic recovery paths, longer supply disruption timelines, and higher ultimate recession risk.

What Griffin’s Warning Means for American Investors and Households

For the investors and households reading this analysis, Griffin’s warning translates into a specific set of practical implications that are worth articulating explicitly.

The six-to-twelve-month clock is already running: The Strait has been effectively closed since March 4, 2026. As of April 14 — the date of Griffin’s remarks — approximately six weeks of closure had already occurred. Griffin’s recession threshold of six to twelve months implies that the point of no return could be reached as early as September 2026. This is not a distant hypothetical — it is a near-term risk horizon with a specific calendar.

The ceasefire condition is necessary but not sufficient: Griffin’s “without tolls, without harassment” criterion means that the April 8 ceasefire, even if it holds, does not eliminate the recession risk he is describing. Markets and households that treat the ceasefire as a clean resolution may be misreading the situation. The economic criterion for resolution is specifically the restoration of full, unencumbered, insurable oil and LNG flow — not merely a cessation of active military hostilities.

Energy-related financial positioning warrants review: Griffin’s conditional recession warning — “if the Strait stays shut for six to twelve months” — is the most analytically relevant framing for investment positioning. Portfolios that are positioned for a rapid return to pre-war normalcy (long cyclical equities, short energy, long consumer discretionary) carry different risk profiles under a six-to-twelve-month closure scenario than under a rapid resolution scenario. Energy equities levered to oil prices, defensive sectors (utilities, healthcare, consumer staples), and inflation-protected assets all merit more favorable positioning under the prolonged closure scenario that Griffin treats as recession-certain.

Emergency financial buffers remain the first-order priority: For households — particularly those in industries most exposed to the adverse scenario (airlines, manufacturing, consumer retail, transportation logistics) — Griffin’s warning reinforces the same practical guidance that flows from every other recession risk assessment in the current environment: build emergency reserves to cover six months of essential expenses, reduce high-rate variable debt, and assess employment exposure to sectors that would face the earliest and sharpest headcount pressure in an energy-shock recession.

Watch the specific economic metric Griffin identified: The single variable Griffin defined as the key criterion — the “resumption of the continued flow of energy products from the Middle East without tolls, without harassment” — is trackable in real time through EIA weekly petroleum supply reports, maritime tracking services (Lloyd’s List, Kpler), and war-risk insurance premium publications. When these indicators confirm full, unencumbered Hormuz transit at pre-war volumes, Griffin’s recession condition has been lifted. Until then, the six-to-twelve-month clock continues.

💬 0 Comments