One of the most common questions Americans ask when recession fears rise is: how long does a recession last? The uncertainty around duration is often more stressful than the downturn itself because households and businesses cannot plan effectively without understanding how long financial hardship might persist. History, fortunately, provides a remarkably clear answer. Since World War II, the United States has experienced 12 officially recognized recessions, and their duration follows patterns that can help every American make smarter financial decisions during periods of elevated economic risk like 2026.

What Officially Defines a Recession?

In the United States, a recession is not defined by the popular shorthand of “two consecutive quarters of negative GDP growth.” The official arbiter of US business cycles is the National Bureau of Economic Research (NBER), a private nonpartisan research organization that has been dating business cycle peaks and troughs since 1854. The NBER’s Business Cycle Dating Committee considers a broad range of economic indicators including nonfarm payroll employment, real personal income less transfers, real personal consumption expenditures, wholesale and retail sales adjusted for price changes, and industrial production. The committee defines a recession as “a significant decline in economic activity that is spread across the economy and lasts more than a few months” (source: nber.org).

This distinction matters for practical planning. The NBER’s definition means that a recession can technically begin even if GDP has not yet turned negative for two quarters, and conversely, GDP can contract for two quarters without the NBER formally declaring a recession if the decline is not sufficiently broad-based across employment, income, and spending data. The committee typically announces recession start and end dates with a significant lag, often 6 to 12 months after the fact, because it waits for sufficient data to confirm that the economy has genuinely shifted direction rather than experiencing temporary volatility.

.

The average US recession since World War II has lasted approximately 10 months from peak to trough. The shortest was the COVID-19 recession at just 2 months; the longest was the Great Recession at 18 months. Understanding historical duration patterns helps you size your emergency fund and plan your investment strategy with realistic expectations.

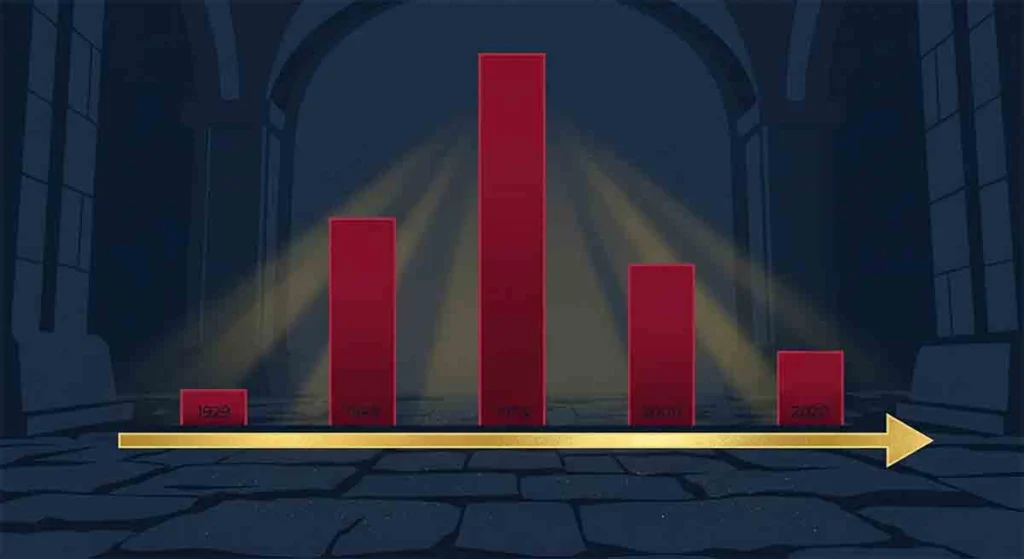

Complete Historical Duration Table: Every US Recession Since 1945

| Recession | Peak | Trough | Duration | GDP Decline |

| Post-WWII | Feb 1945 | Oct 1945 | 8 months | -11.6% |

| 1948-49 | Nov 1948 | Oct 1949 | 11 months | -1.7% |

| 1953-54 | Jul 1953 | May 1954 | 10 months | -2.2% |

| 1957-58 | Aug 1957 | Apr 1958 | 8 months | -3.7% |

| 1960-61 | Apr 1960 | Feb 1961 | 10 months | -1.6% |

| 1969-70 | Dec 1969 | Nov 1970 | 11 months | -0.6% |

| 1973-75 | Nov 1973 | Mar 1975 | 16 months | -3.2% |

| 1980 | Jan 1980 | Jul 1980 | 6 months | -2.2% |

| 1981-82 | Jul 1981 | Nov 1982 | 16 months | -2.7% |

| 1990-91 | Jul 1990 | Mar 1991 | 8 months | -1.4% |

| 2001 | Mar 2001 | Nov 2001 | 8 months | -0.3% |

| Great Recession | Dec 2007 | Jun 2009 | 18 months | -4.3% |

| COVID-19 | Feb 2020 | Apr 2020 | 2 months | -9.1% (Q2) |

Source: National Bureau of Economic Research (nber.org/research/data/us-business-cycle-expansions-and-contractions). The average duration across all 13 post-WWII recessions is approximately 10 months. The median is also approximately 10 months, which indicates that the distribution is relatively symmetric and that the 10-month average is not being distorted by extreme outliers.

What Factors Determine How Long a Recession Lasts?

Not all recessions are created equal. The duration of a recession depends on four primary factors that interact in complex ways.

Root cause matters enormously. Recessions triggered by financial crises — such as the Great Recession of 2007-2009, which was caused by a systemic collapse in mortgage-backed securities and banking solvency — tend to last significantly longer than recessions caused by external shocks. The Great Recession lasted 18 months and required years of additional recovery because the banking system itself was impaired, meaning credit could not flow normally even after the recession technically ended. By contrast, the COVID-19 recession lasted only 2 months because the underlying cause was an external public health shock rather than a structural economic failure, and the economy was able to rebound quickly once policy support arrived.

Policy response speed and scale are critical determinants. The Federal Reserve’s ability to cut interest rates rapidly, deploy quantitative easing, and create emergency lending facilities has shortened modern recessions dramatically compared to pre-Federal Reserve downturns. According to Federal Reserve Economic Data (FRED) maintained by the Federal Reserve Bank of St. Louis (fred.stlouisfed.org), pre-WWII recessions averaged approximately 21 months compared to 10 months post-WWII. The 2020 recession illustrates the extreme case: the combination of $2.2 trillion in CARES Act fiscal stimulus, Federal Reserve balance sheet expansion from $4 trillion to $9 trillion, enhanced unemployment benefits, PPP loans, and direct stimulus payments produced the shortest recession in recorded US history.

Consumer and business debt levels influence recession depth and duration. When households enter a recession with high debt-to-income ratios, the downturn tends to persist longer because consumers must simultaneously reduce spending and service debt obligations. The Federal Reserve Bank of New York’s Household Debt and Credit Report tracks total household debt, which reached $18.04 trillion in Q4 2025 — a figure worth monitoring as recession risk rises in 2026.

Banking system health determines how quickly credit can resume flowing to consumers and businesses after a downturn. Recessions accompanied by banking crises (1990-91 savings and loan crisis, 2007-2009 mortgage crisis) produce longer recoveries because the financial intermediation necessary for economic activity is impaired even after other conditions improve.

Pre-WWII vs. Post-WWII: Why Modern Recessions Are Shorter

The dramatic improvement in recession duration from the pre-WWII to post-WWII era is one of the most important and underappreciated developments in American economic history. Before 1945, the average recession lasted approximately 21 months. After 1945, the average fell to 10 months. This improvement reflects four structural changes in the US economy.

First, the Federal Reserve, though established in 1913, was significantly empowered by the Banking Acts of 1933 and 1935 and has since developed sophisticated tools for monetary intervention. Modern central banking gives policymakers the ability to cut interest rates, inject liquidity into financial markets, and serve as a lender of last resort to prevent financial panics from cascading into prolonged depressions.

Second, automatic fiscal stabilizers were created during the New Deal era and expanded over subsequent decades. Unemployment insurance, established in 1935, automatically provides income to displaced workers without requiring new legislation. Social Security, also established in 1935, maintains retirement income regardless of economic conditions. The Supplemental Nutrition Assistance Program (SNAP), Medicaid, and the Earned Income Tax Credit all inject spending into the economy precisely when private-sector spending contracts.

Third, the Federal Deposit Insurance Corporation (FDIC), created in 1933, eliminated the phenomenon of bank runs that turned garden-variety recessions into catastrophic depressions throughout the 19th and early 20th centuries. Before the FDIC, a rumor about a bank’s solvency could trigger mass withdrawals that destroyed solvent banks and wiped out depositors’ savings, creating cascading failures across the financial system. FDIC insurance covering up to $250,000 per depositor per bank has made this dynamic virtually impossible in the modern era (source: fdic.gov).

Fourth, the sheer diversity and scale of the modern US economy provide built-in resilience. A $28 trillion economy spanning agriculture, manufacturing, services, technology, healthcare, and finance is structurally less vulnerable to sector-specific shocks than the smaller, more concentrated economy of the pre-WWII era.

What Would a 2026 Recession Duration Look Like?

If a recession materializes in 2026, economists generally project a mild-to-moderate downturn lasting 6 to 12 months. Several factors support this projection. The US labor market, while softening, entered 2026 from a position of relative strength with unemployment below 5%. The Federal Reserve retains significant room to cut interest rates from their current level, providing conventional monetary policy ammunition. The banking system, stress-tested annually under Dodd-Frank requirements, is significantly better capitalized than it was in 2007.

However, a 12 to 18 month scenario cannot be ruled out if multiple negative factors compound simultaneously. The ongoing geopolitical conflict involving Iran and the Strait of Hormuz has elevated oil prices, which historically precede longer downturns. Tariff-driven inflation constrains the Federal Reserve’s ability to cut rates aggressively because rate cuts that stimulate demand could simultaneously worsen inflation. Consumer credit card debt has reached record levels, reducing households’ financial cushion. If these factors converge with a meaningful weakening in the labor market, the resulting downturn could extend toward the upper end of the historical range.

For planning purposes, the most prudent approach is to prepare for a 12-month recession while hoping for a shorter one. This means maintaining at least 6 months of essential expenses in an emergency fund, avoiding new non-essential debt, and ensuring your investment portfolio is diversified across asset classes that perform differently during economic contractions (see: investor.gov for general investment planning guidance from the SEC).

How to Use Historical Duration Data in Your Financial Plan

Understanding recession duration is not an academic exercise — it has direct, actionable implications for how you structure your finances. The 10-month average tells you that your emergency fund should cover at minimum 6 months of essential expenses, with 9 to 12 months providing a stronger cushion for higher-risk households (single-income families, workers in cyclical industries, self-employed individuals). The Bureau of Labor Statistics reports that the median duration of unemployment rises significantly during recessions — from approximately 9 weeks during expansions to 15 to 25 weeks during downturns — which directly informs how much liquidity you need (source: bls.gov/cps).

For investors, the historical data shows that stock market recoveries typically begin 3 to 6 months before the recession officially ends, as markets are forward-looking. Selling investments during a recession often means locking in losses right before the recovery begins. The S&P 500 has recovered from every recession in US history, and investors who remained invested through downturns have consistently outperformed those who sold during panic.

The key takeaway is straightforward: recessions are temporary. The average modern recession lasts less than one year. Every recession in the post-WWII era has been followed by an expansion that lasted longer and produced more economic growth than the recession destroyed. Planning for a finite, historically bounded period of economic difficulty is fundamentally different from planning for permanent decline — and the data overwhelmingly supports the former.

💬 0 Comments